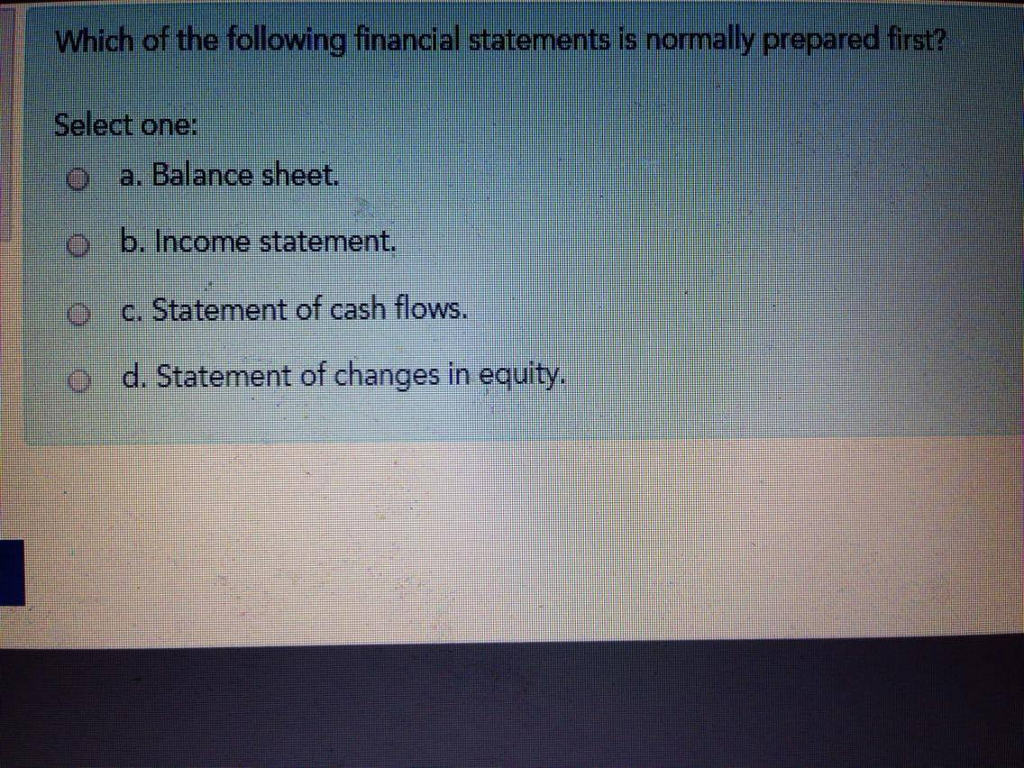

Which Of The Following Financial Statements Should Be Prepared First

Let's talk about something that might sound a little dry – financial statements. But trust me, understanding them, and especially knowing which one to prepare first, is like unlocking a secret code to managing your money better. Whether you're a complete beginner, a family trying to budget, or just someone who enjoys a good spreadsheet, this knowledge is surprisingly powerful.

So, which statement takes the lead? The answer is the Income Statement (sometimes called the Profit and Loss Statement). Think of it like this: before you know where you stand financially (your balance sheet), and before you know how cash is flowing (cash flow statement), you need to understand how you're performing. The income statement shows you exactly that – are you making a profit or taking a loss?

Why the Income Statement First? For beginners, it's the most intuitive. It's simply your revenue (money coming in) minus your expenses (money going out) over a specific period (like a month, quarter, or year). Seeing this laid out clearly allows you to quickly identify areas where you might be overspending or where you could potentially increase your income. It's the foundation for understanding your financial health.

Must Read

For families, this is invaluable for budgeting. An income statement lets you track your household income (salaries, investments, etc.) and compare it to your household expenses (groceries, rent, utilities, entertainment). Seeing this difference helps you create a realistic budget and identify areas where you can save for important goals, like a vacation or a down payment on a house. You can even break down expenses into categories to see where your money is truly going – are you spending too much on eating out?

For hobbyists or small business owners, a simple income statement can be a lifesaver come tax time. By tracking your income from your hobby (selling crafts, tutoring, etc.) and deducting related expenses (supplies, marketing), you can accurately report your profit or loss. Plus, it gives you valuable insights into whether your hobby is actually a profitable venture!

Variations and Examples: A very simple income statement might just list total income and total expenses. A more detailed one could break down income by source (salary, freelance work) and expenses by category (housing, transportation, food). For a small business, it might include cost of goods sold and gross profit calculations.

Getting Started: Don't be intimidated! You don't need fancy software. Start with a simple spreadsheet. List your income sources in one column and your expenses in another. Subtract the total expenses from the total income. Voila! You have a basic income statement. Track this regularly (monthly is a good start) and you'll be amazed at how much better you understand your finances.

![[SOLVED] The following financial statements were prepared on December](https://dsd5zvtm8ll6.cloudfront.net/si.question.images/image/images7/464-B-A-C(622).png)

Practical Tips: Use online banking to easily track your income and expenses. Categorize your expenses as you go, rather than trying to remember where your money went at the end of the month. Consider using budgeting apps that automatically categorize your transactions.

Ultimately, understanding your financial performance starts with the Income Statement. It's a powerful tool that allows you to take control of your money, achieve your financial goals, and maybe even discover a hidden talent for financial wizardry! So, embrace the spreadsheet, track those numbers, and enjoy the journey to a more financially secure future.