Where To Start Buying A House

Ever caught yourself scrolling through dreamy house pictures online, perhaps on a lazy Sunday afternoon, and wondered, "Could I actually do this?" Or maybe you've been renting for a while, and the thought of putting your hard-earned cash into something you can truly call your own has started to bubble up. Buying a house might seem like a giant, intimidating mountain to climb, full of confusing jargon and endless paperwork. But guess what? It doesn't have to be!

Think of it less like a scary financial Everest expedition and more like planning an epic road trip. You wouldn't just jump in the car without a map, right? Or at least a vague idea of where you're headed and what snacks you'll need. Starting the journey to homeownership is surprisingly similar. It's about curiosity, planning, and a bit of fun dreaming. So, where on earth do you even begin?

Let's Get Curious: What's Your Home Vibe?

Before you even think about saving a penny or looking at mortgage rates, the absolute coolest place to start is with your imagination. Seriously! This is the fun part. What does your ideal living situation even look like?

Must Read

Are you picturing a cozy bungalow with a porch swing for sipping lemonade? Or maybe a sleek, modern condo in the heart of the city, perfect for grabbing a late-night bite? Perhaps a sprawling backyard for your furry friends (or future garden projects!) is non-negotiable.

This isn't just daydreaming; it's crucial groundwork. Think about your lifestyle. Do you love to entertain? Then an open-plan living area might be high on your list. Are you a homebody who craves a quiet sanctuary? Maybe a home tucked away from the hustle and bustle is more your speed. Consider the number of bedrooms, the commute to work, proximity to parks, schools, or your favorite coffee shop.

It’s a bit like deciding what kind of vacation you want before booking flights. Do you want a relaxing beach resort, an adventurous mountain trek, or a cultural city break? Each requires a different kind of planning, and so does finding your perfect home. Don't rush this stage; it helps clarify what you're truly looking for.

The Money Talk (Made Less Scary!)

Okay, the dreaming is done (for now!). Let's gently nudge into the financial side. Don't groan! This part is empowering because it tells you what's realistic and what's still a dream to work towards.

Understanding Your Wallet: What Can You Afford?

This is perhaps the most important practical step. Buying a house isn't just about the sticker price; it's about the entire financial picture. Think of it like buying a new car: there's the monthly payment, but also insurance, gas, and maintenance. Houses are similar, but with more zeros!

Start by getting a really honest look at your income and expenses. What's coming in, and what's going out? This isn't just about how much you can afford for a monthly mortgage payment, but also accounting for property taxes, homeowners insurance, potential HOA (Homeowners Association) fees, and the inevitable maintenance costs.

A great rule of thumb is the 28/36 rule, which suggests that your housing costs shouldn't exceed 28% of your gross monthly income, and your total debt payments (including housing) shouldn't exceed 36%. It's a guideline, not a law, but it's a solid starting point for budgeting.

Your Financial Report Card: The Credit Score

Your credit score is like your financial GPA. Lenders look at it to see how reliable you are at paying back debts. A higher score generally means better interest rates on your mortgage, which can save you thousands over the life of the loan.

Don't know your score? Now's the time to find out! You can usually get a free annual report from the major credit bureaus. If it's not where you want it to be, don't fret. There are plenty of resources out there to help you improve it by making on-time payments and managing your existing debt. Think of it as studying for a big test – a little effort now can pay off big later.

The Down Payment Dilemma (or Opportunity!)

The down payment is often the biggest hurdle, but it's also a huge advantage. It's the chunk of cash you pay upfront for the house, and it directly reduces the amount you need to borrow. While the traditional 20% down payment is ideal (it often helps you avoid private mortgage insurance, or PMI), many loan programs allow for much less, sometimes as low as 3.5% or even 0% for certain types of loans (like VA loans for veterans).

Start a dedicated savings fund, even if it's just a small amount each month. Every little bit counts. Automate transfers, cut back on non-essentials, and maybe even pick up a side hustle. It's a marathon, not a sprint, and watching that fund grow is incredibly motivating!

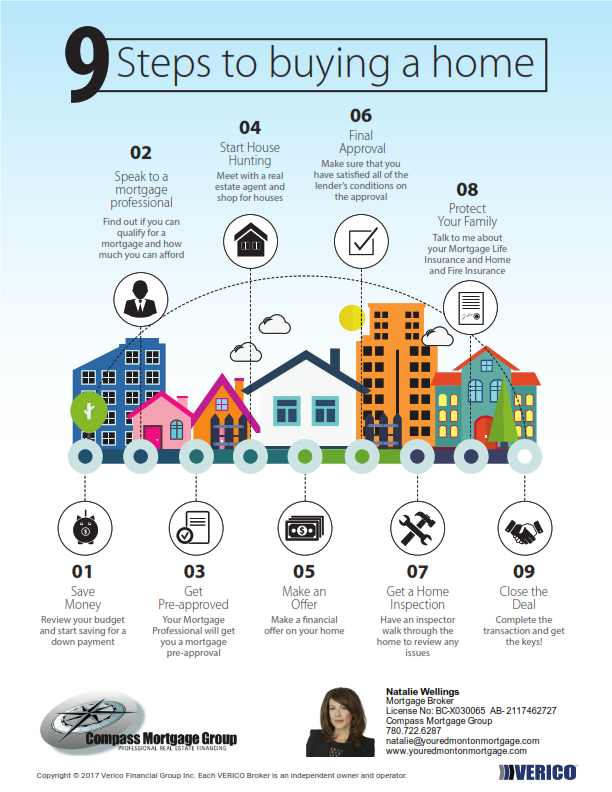

Getting Your Golden Ticket: Pre-Approval

Once you have a clearer picture of your finances, the next super important step is to get pre-approved for a mortgage. This isn't the same as pre-qualification; pre-approval means a lender has actually reviewed your financial documents (income, assets, credit) and determined exactly how much they are willing to lend you.

Think of it as getting your "golden ticket" to start seriously looking at houses. Not only does it show sellers you're a serious buyer (which is a huge advantage in a competitive market!), but it also gives you a firm budget to work with. No more guessing games! You'll know your price range and can focus your search effectively.

This is also a great time to shop around for lenders. Don't just go with the first bank you see! Different lenders offer different rates and terms, so comparing a few can save you a bundle over time. It's like comparing prices for a big purchase – you want the best deal, right?

Your Real Estate Guru: Finding an Agent

With your finances in order and your pre-approval in hand, it’s time to find your guide for this adventure: a real estate agent. A good agent is your advocate, your source of local knowledge, and your negotiator. They'll help you navigate the market, find homes that match your criteria, and walk you through the entire process, from making an offer to closing the deal.

Look for someone who understands your needs, communicates well, and has a great reputation. Ask friends for recommendations, read reviews, and interview a few different agents until you find someone you click with. This person will be your trusted partner, so choose wisely!

The Big Takeaway: Enjoy the Journey!

See? It’s not so scary after all! Starting the journey to buying a house is less about jumping into the deep end and more about a series of curious explorations and sensible steps. From dreaming up your ideal home vibe to understanding your finances and getting pre-approved, each step builds confidence and clarity.

Embrace the process. Ask questions. Learn as you go. It's an exciting adventure towards a significant milestone in your life. And remember, every homeowner started exactly where you are right now: at the very beginning, wondering where to start. So, take a deep breath, get curious, and enjoy mapping out your very own road trip to homeownership!