What Requirements Are Needed To Buy A House

So, you're thinking about buying a house? Awesome! It's a big step, like leveling up in your favorite game. But before you start packing your imaginary boxes, let's chat about what you actually need to make it happen. It's not as scary as it sounds, promise! Think of this as your friendly guide to unlocking homeownership.

The Foundation: Your Credit Score

First up, let's talk about your credit score. This little number is basically your financial report card. Lenders use it to gauge how likely you are to pay them back. A higher score is like having a cheat code – it opens the door to better interest rates and loan options.

Think of it this way: Your credit score is like your reputation at a neighborhood bake sale. If you always bring delicious cookies and pay on time, everyone trusts you! But if you show up empty-handed and "forget" to pay, well… they might be a little hesitant to let you borrow their mixing bowl. Aim for a score of 620 or higher for most mortgages. The higher, the better!

Must Read

Money, Money, Money: Down Payment and More

Now, let's tackle the big one: the down payment. This is the chunk of cash you put down upfront. Traditionally, 20% was the magic number, but these days, there are plenty of options with much lower down payments, sometimes even as low as 3%!

Imagine you're buying a giant, inflatable unicorn sprinkler (because why not?). A 20% down payment is like paying for the horn and mane upfront. But with a lower down payment option, you might only need to cover the unicorn's tail. Makes it a bit more manageable, right?

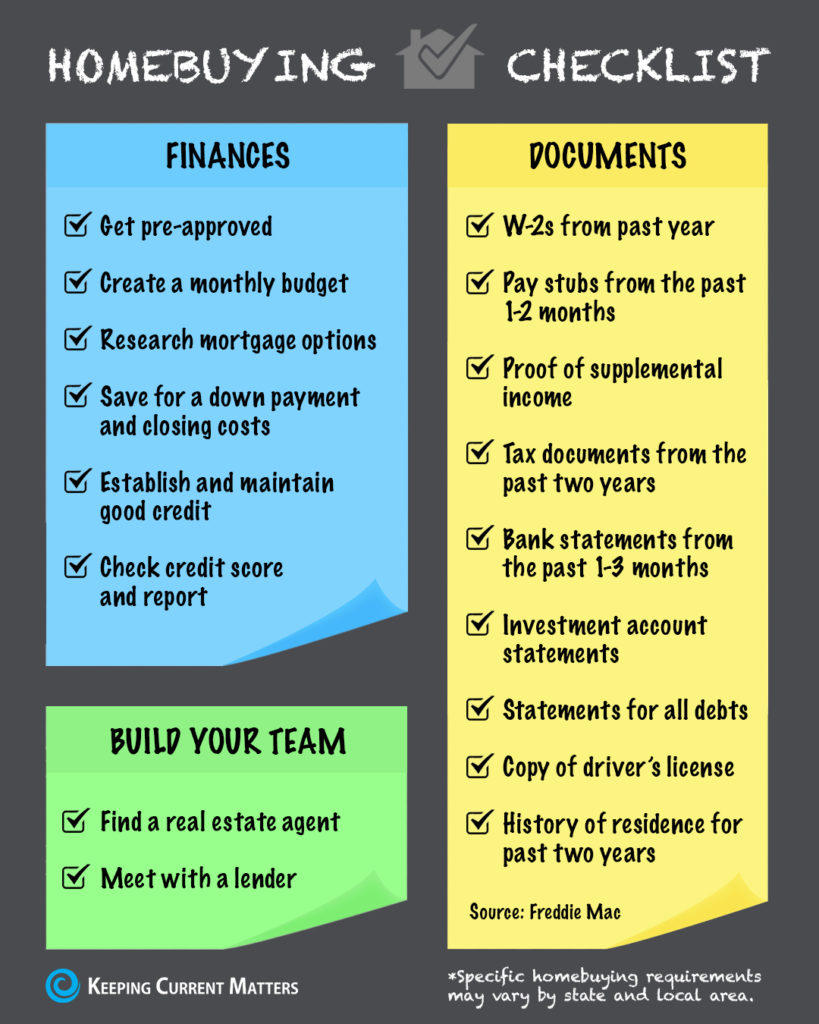

But wait, there's more! Don't forget about closing costs. These are fees associated with the loan and the transfer of ownership. Think of them as the fine print on your unicorn sprinkler warranty. They can include things like appraisal fees, title insurance, and taxes. Factor these into your budget – they can add up!

Proof You Can Pay: Income and Employment

Lenders want to know you can actually afford to pay back the loan. Makes sense, right? They'll want to see proof of your income, typically through pay stubs, W-2s, and tax returns. They'll also look at your employment history to see how stable your job is.

This is like showing the bake sale committee your award-winning recipe and a photo of you successfully baking that cake 100 times. You’re demonstrating your ability to deliver!

Debt-to-Income Ratio: Keeping it Real

Speaking of affordability, lenders will also calculate your debt-to-income ratio (DTI). This is basically how much of your monthly income goes towards paying off debts like credit cards, student loans, and car payments. A lower DTI is better because it shows you have more wiggle room in your budget.

Think of your DTI as your backpack on a hiking trip. If it's stuffed to the brim with heavy rocks (lots of debt!), it's going to be a tough climb. But if it's light and streamlined (low debt!), you'll have a much easier time reaching the summit (homeownership!).

Pre-Approval: Your Secret Weapon

Before you start house hunting, get pre-approved for a mortgage. This is like getting a golden ticket that tells you exactly how much a lender is willing to loan you. It gives you a realistic budget and makes you look super serious to sellers. Plus, it streamlines the whole process when you find "the one."

Getting pre-approved is like having a VIP pass to the best amusement park ride (buying a house!). You get to skip the long lines (bidding wars!) and jump straight to the fun part (owning your home!).

Patience is Key: The Home Buying Journey

Finally, remember that buying a house is a process. There will be paperwork, negotiations, and maybe a few moments of stress. But with a little planning and the right guidance, you can totally nail it!

It's like learning a new skill, like riding a unicycle. You might wobble and fall a few times, but eventually, you'll be cruising down the street with a smile on your face (and a house key in your pocket!).

So, are you ready to take the plunge? You got this!