What Is The Credit Card Billing Cycle

:max_bytes(150000):strip_icc()/billing-cycle-960690-color-v01-43af5d5ef90e46d6b3484e6900ba827a.png)

Ever wonder how your credit card seems to magically tally up your spending each month, presenting you with a neat little bill? Or how you manage to avoid interest when you pay on time? It all boils down to something wonderfully simple yet incredibly powerful: the credit card billing cycle. Understanding this little financial rhythm isn't just about being a responsible adult; it's like learning the secret handshake to smarter money management, and frankly, it's pretty fascinating!

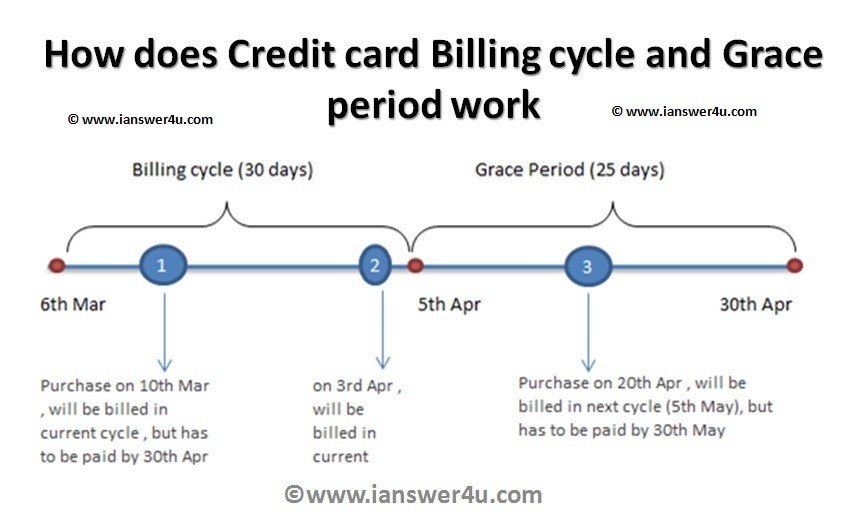

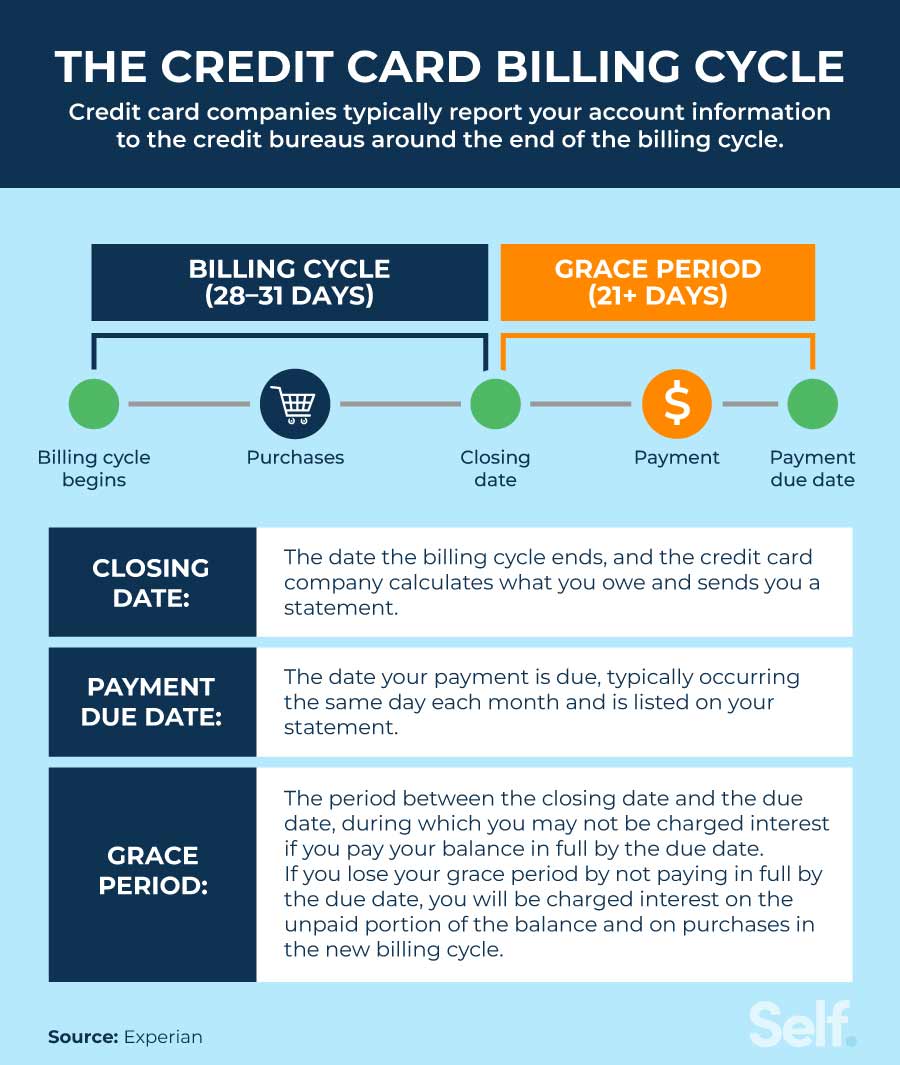

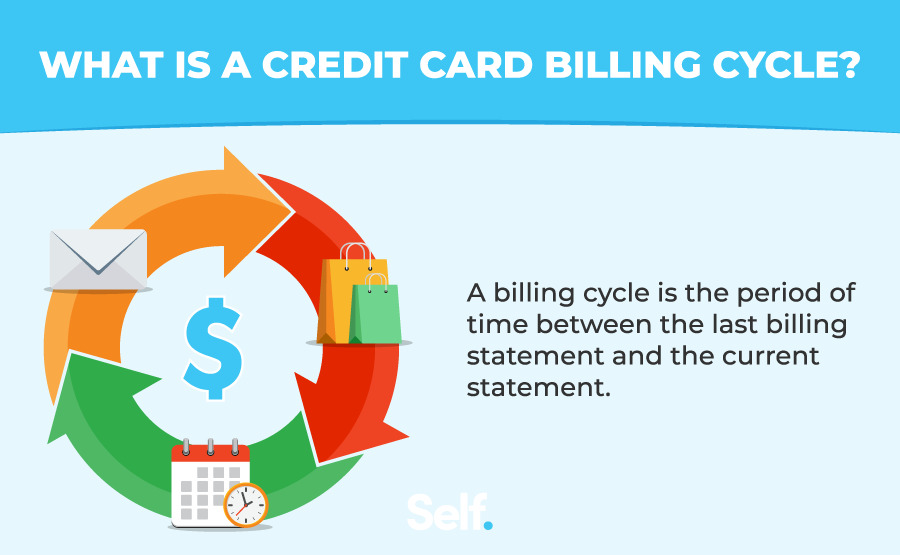

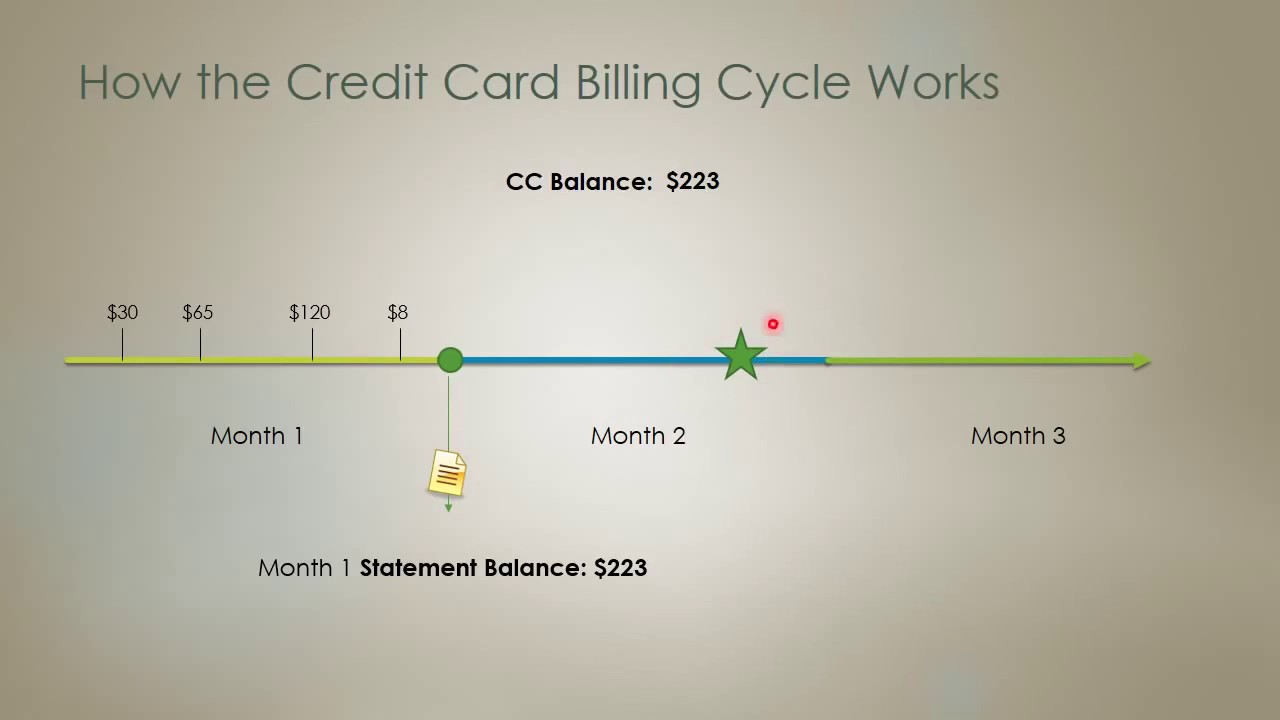

So, what exactly is this mystical cycle? At its core, the billing cycle is simply the period of time between one credit card statement and the next. Think of it as a financial month, often lasting between 28 and 31 days, depending on your card issuer. During this period, all your purchases, payments, and any fees are recorded. At the end of the cycle, your card issuer generates a statement that summarizes everything, along with your minimum payment due and the all-important payment due date.

The purpose? It's all about clarity and control! This structured cycle provides a clear snapshot of your spending, making it much easier to budget and track where your money goes. One of its greatest benefits is enabling the grace period. This is the magical window – usually between 21 and 25 days – from your statement closing date until your payment due date. If you pay your entire statement balance in full before or on that due date, you pay zero interest on new purchases. It’s essentially an interest-free loan for nearly a month and a half, provided you play by the rules! Beyond saving you money on interest, understanding the cycle helps you build a strong credit history through timely payments and allows you to maximize rewards by timing larger purchases strategically.

Must Read

Let's look at it in action. Imagine your billing cycle closes on the 10th of every month, and your payment is due on the 5th of the following month. If you make a big purchase on the 11th, right after your statement closes, that purchase won't appear on this month's statement. Instead, it'll show up on next month's statement, giving you almost two full months before you need to pay for it without incurring interest – a fantastic trick for managing cash flow for bigger expenses! Conversely, if you make a purchase on the 9th, it will appear on the current statement, and you'll need to pay for it by the upcoming due date. This distinction is vital for avoiding surprises and late fees.

Ready to explore your own billing cycle? It's super easy! First, log into your online credit card account or look at a physical statement. Find your statement closing date (sometimes called the cycle end date) and your payment due date. Mark these on your calendar! A great tip is to set reminders a few days before your payment is due, giving you ample time to pay and avoid any late fees. To truly grasp it, try making a small purchase right after your statement closes, and another right before it closes. Observe how they appear on subsequent statements. Always aim to pay your full statement balance every single month to fully leverage the grace period and keep interest charges at bay. Understanding this simple cycle transforms your credit card from a mysterious money tool into a powerful personal finance ally.