What Is Penalty For 401k Early Withdrawal

Alright, folks, let's talk about something super important but often shrouded in mystery: dipping into your 401(k) early. Imagine your 401(k) as a delicious cake you're baking for a special occasion.

Taking a slice before it's done? Not only will it taste kinda weird, but you'll also face some consequences. We're talking about the dreaded early withdrawal penalties!

The 10% Taxman Cometh!

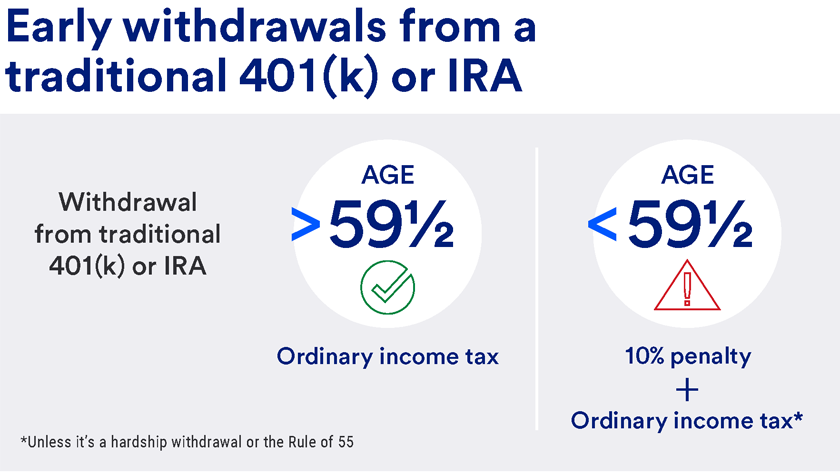

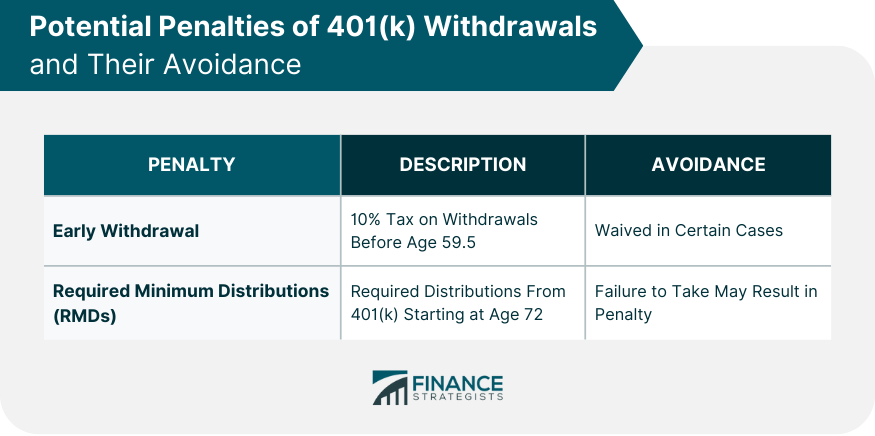

Here's the deal: if you withdraw money from your 401(k) before you reach age 59 ½, Uncle Sam is gonna want his cut. And by "cut," I mean a hefty 10% penalty on top of the regular income tax you'll owe.

Must Read

Think of it like this: you're throwing a party and forgetting to invite the taxman. He will find out, and he will bring the awkward vibes.

So, let’s say you’re staring down a financial emergency and decide to yank out $10,000 from your retirement savings. Ouch! That's a tough decision.

Prepare for the one-two punch: a 10% penalty, which is $1,000 gone right off the bat, plus regular income tax on the entire $10,000, depending on your tax bracket.

Suddenly, that $10,000 doesn’t look so big, does it? It shrinks faster than a wool sweater in a hot dryer!

Regular Income Tax – The Other Shoe Drops

Don’t forget about this one! Your 401(k) contributions were likely made with pre-tax dollars.

That means you didn’t pay income tax on that money when you earned it. Now that you're withdrawing it, the government wants its due.

This amount will depend on your individual tax bracket that year, and it can significantly reduce the amount you actually take home.

Imagine winning a lottery, only to discover that half of your winnings vanish due to taxes. That’s kind of what it feels like.

So, How Big of a Deal is This, Really?

A huge deal! Taking money out of your 401(k) early isn't just about the immediate penalties. It's about sacrificing your future financial security.

Think of your 401(k) as a little money tree that's growing over time. Each withdrawal is like chopping off a branch. It stunts the growth and reduces the fruit (retirement income) you'll eventually harvest.

Compounding is the magic that makes your retirement savings grow exponentially. The longer your money stays invested, the more it earns.

Every dollar you withdraw early isn't just gone; it's the potential future earnings that are also lost. It’s like killing a golden goose for a single, quickly-spent egg!

Are There Any Exceptions? (A Glimmer of Hope!)

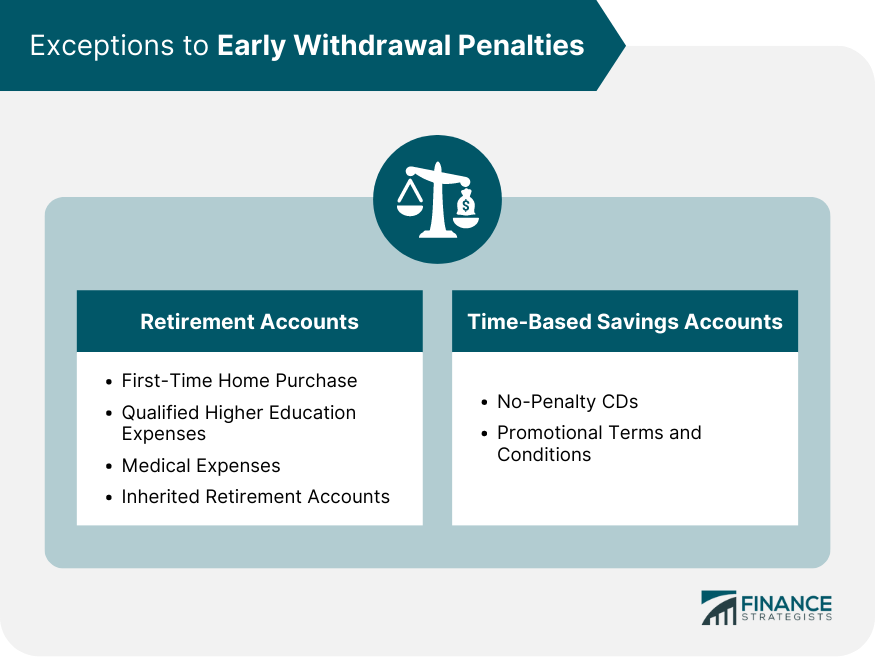

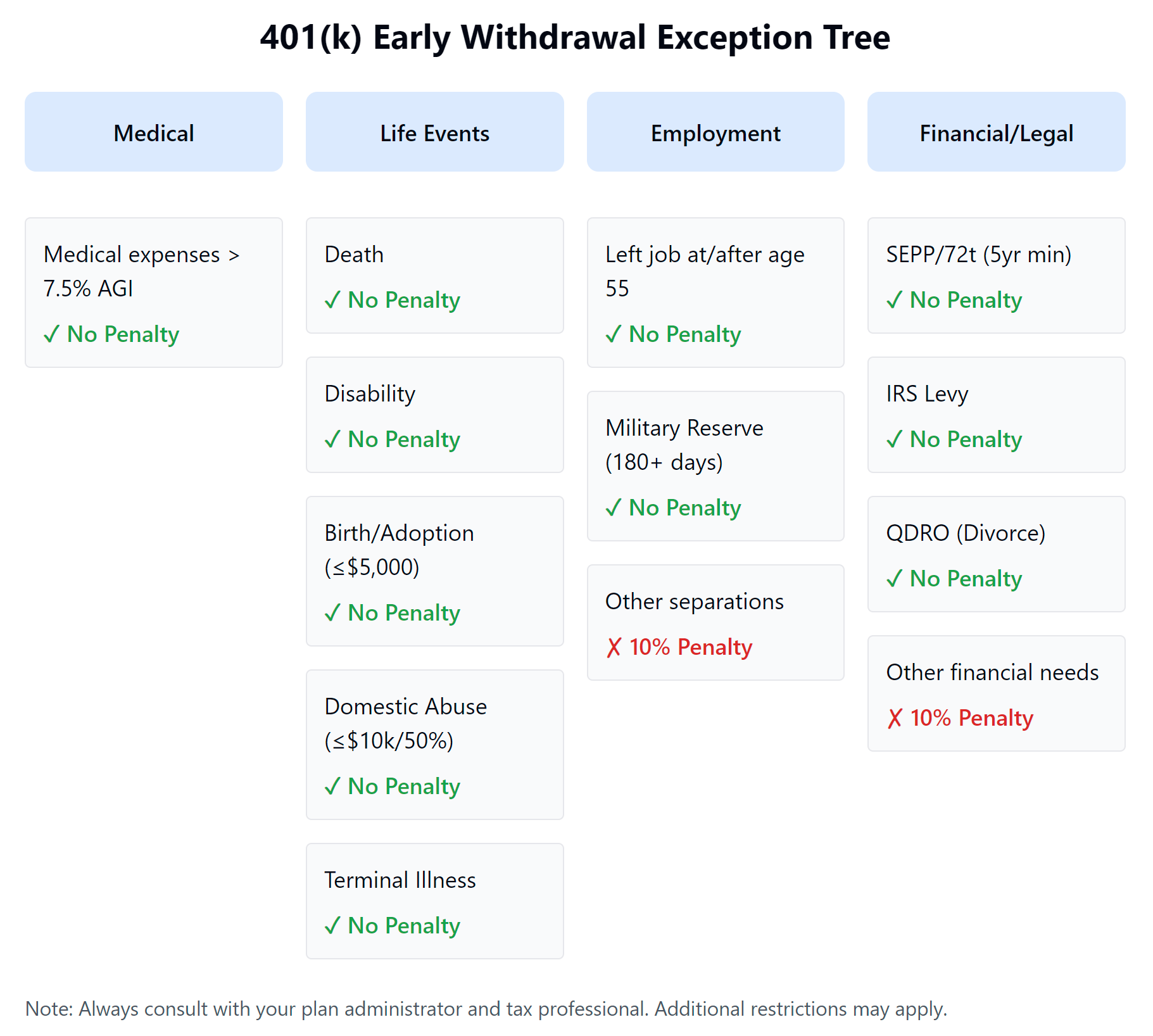

Okay, it’s not all doom and gloom! The government, in its infinite wisdom, does provide a few exceptions to the early withdrawal penalty.

These exceptions are generally for dire circumstances, and they come with their own set of rules and stipulations, so it's crucial to do your homework.

Think of these exceptions as secret passages in a financial labyrinth. They exist, but you need a map and a guide to navigate them safely!

Common Exceptions to the 10% Penalty:

Here are a few of the most common exceptions, but remember, these often have specific requirements:

Unreimbursed Medical Expenses: If you have significant medical bills that exceed a certain percentage of your adjusted gross income, you might be able to withdraw penalty-free.

Disability: If you become permanently and totally disabled, you can often access your 401(k) funds without penalty.

Qualified Domestic Relations Order (QDRO): In a divorce, a QDRO can allow for the division of retirement assets without triggering a penalty.

IRS Levy: If the IRS levies your 401(k), you won't be penalized for the withdrawal.

Death: Your beneficiaries won't be penalized when they inherit your 401(k) (although they will likely owe income tax).

401(k) Withdrawal Tax for Nonresidents | Finance Strategists

Some plans may also offer loans, which can be a better option than an early withdrawal, if you are able to pay it back.

These exceptions are complicated, so always consult with a qualified tax advisor or financial planner to determine if you qualify. Don't rely solely on this article!

Alternatives to Early Withdrawal

Before you even think about touching your 401(k), explore all other options! Desperate times call for creative solutions, not hasty decisions that can jeopardize your future.

Imagine your 401(k) as your last resort. Use up everything else before reaching for it!

Here are some alternatives to consider:

Emergency Fund: This is what it's there for! If you have an emergency fund, now is the time to use it.

Cut Expenses: Look for ways to reduce your spending. Even small cuts can make a big difference.

Sell Assets: Consider selling non-essential assets, like a second car or valuable collectibles.

Debt Counseling: If you're struggling with debt, a credit counselor can help you create a budget and negotiate with creditors.

Borrowing: Explore options like a personal loan or a home equity loan.

The Bottom Line

Withdrawing from your 401(k) early is a serious decision that should only be made as a last resort. The penalties and taxes can significantly reduce the amount you receive, and you'll be sacrificing your future financial security.

Think of it like breaking the piggy bank you've been diligently filling for years. Once it's broken, it's hard to put the pieces back together!

Before you raid your retirement nest egg, explore all other alternatives and consult with a financial professional. Your future self will thank you!

Remember, patience is a virtue, especially when it comes to retirement savings. Your 401(k) is your ticket to a comfortable and secure future. Guard it wisely!

So, let's keep that cake in the oven until it's fully baked and ready to be enjoyed. Your future self deserves a delicious and well-deserved retirement!