What Do I Need To Open A Bank Account Citibank

Alright, settle in, grab your metaphorical latte, and let’s chat about opening a bank account at Citibank. It’s not rocket science, but sometimes feels like you need a PhD in "Bureaucratic Jargon Comprehension" to navigate the process. Don't worry, I’m here to be your translator – think of me as the Rosetta Stone for banking. Let’s dive in!

First Things First: Proof You’re Not a Figment of My Imagination

Okay, before Citibank lets you waltz in and start depositing your hard-earned cash (or, let’s be real, that birthday money Grandma sent), they need to make sure you’re actually, you know, real. This involves showing them some official documentation. Think of it as proving you’re not just a particularly convincing mirage in the desert of finance.

So, what proof do you need? Buckle up!

Must Read

- Photo ID, Glorious Photo ID! This is your golden ticket. We’re talking driver’s license, passport, state-issued ID – something with your picture on it that screams, "Yes, this is me! I exist! And I haven't used a filter!" They typically accept various types but confirm what is acceptable on their website or call to be extra safe.

- Proof of Address: Where Do You Hang Your Hat (and Deposit Your Mail)? They need to know where to send those oh-so-exciting bank statements (said no one, ever). A utility bill (electricity, water, gas), a lease agreement, or even a piece of official mail addressed to you at your current abode will do the trick. Just make sure it's relatively recent. A postcard from your aunt Edna from 1998 won't cut it.

- Social Security Number or ITIN: The Numbers Game. This is how the government keeps track of your financial comings and goings. Think of it as your financial fingerprint. If you don’t have a Social Security Number, an Individual Taxpayer Identification Number (ITIN) is also acceptable in many cases.

Important Note: Make sure these documents are originals or certified copies. A blurry photo of your driver's license taken with a potato might not inspire confidence.

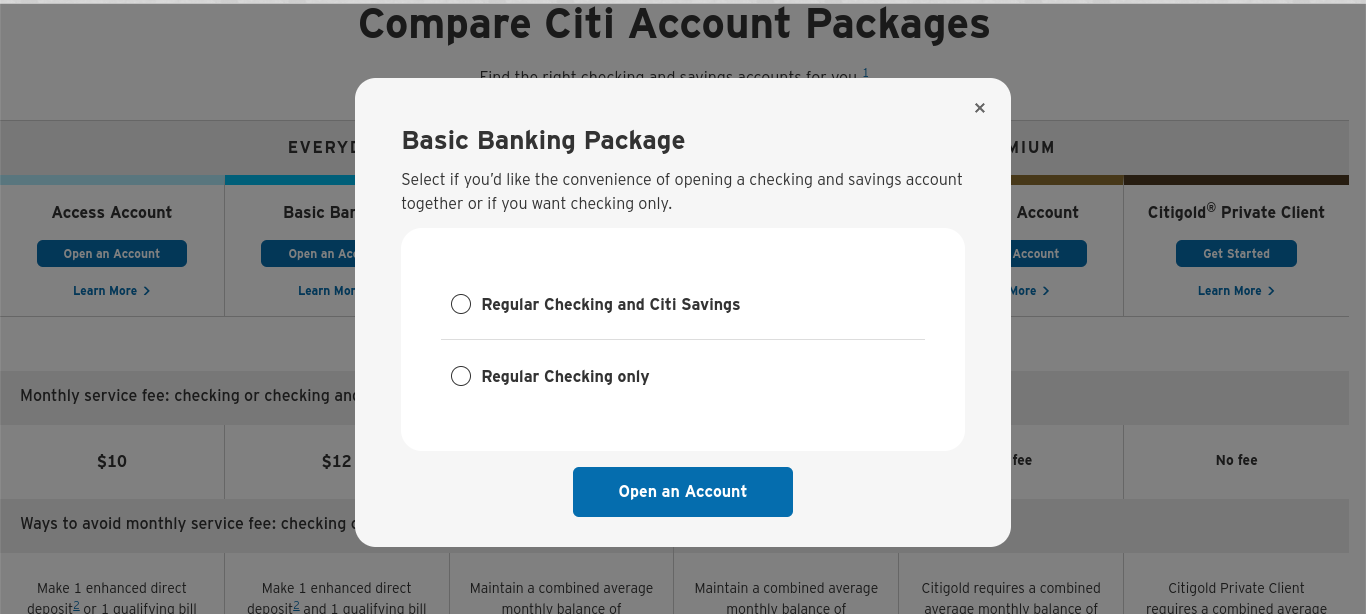

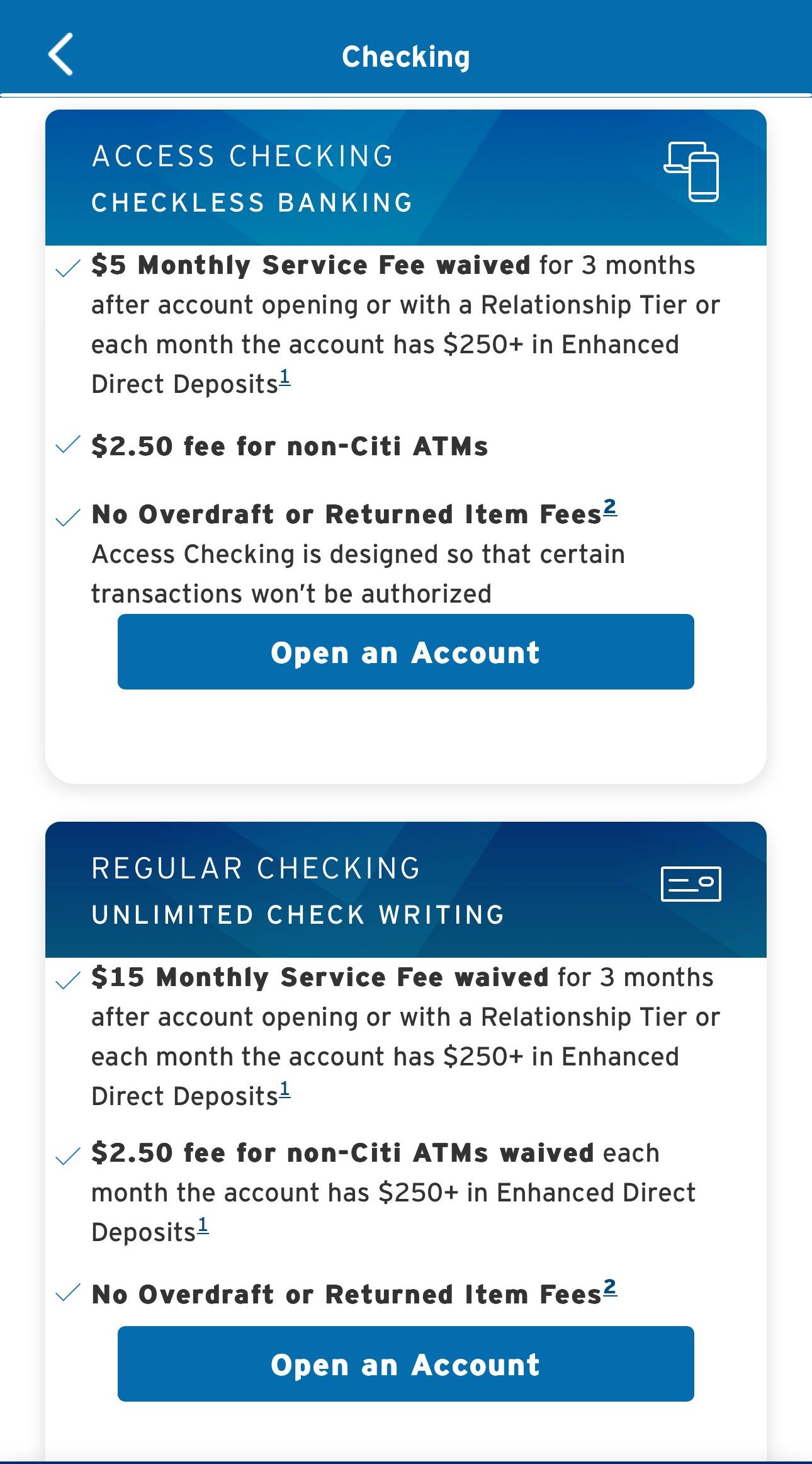

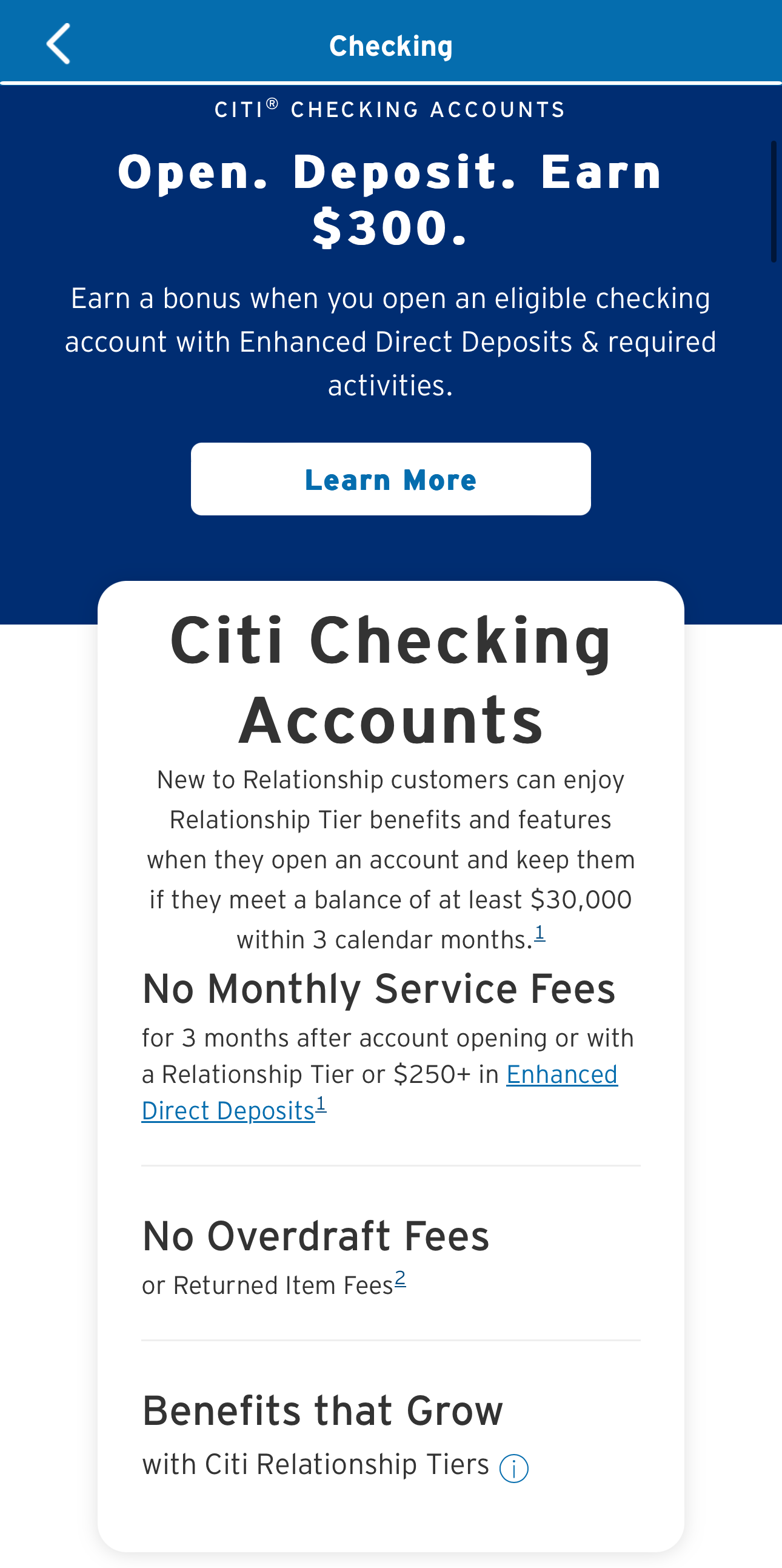

Choosing Your Financial Adventure: Account Types Galore

Citibank, like most banks, offers a whole buffet of account types. It’s like walking into an ice cream shop with 31 flavors – overwhelming, but ultimately delicious (hopefully!). Here’s a quick rundown of some common suspects:

- Checking Account: This is your everyday workhorse. For paying bills, swiping your debit card for that late-night pizza run, and generally managing your funds.

- Savings Account: Where you stash your cash for a rainy day (or that impulse buy you’ve been eyeing). It earns a tiny bit of interest, though let's be honest, you won't be retiring on it.

- Money Market Account: A hybrid of checking and savings, often offering slightly higher interest rates, but may require a higher minimum balance.

- CDs (Certificates of Deposit): You lock your money away for a specific period (like a financial time capsule) and earn a guaranteed interest rate. Just don't try to break into that time capsule early – you'll face penalties!

Choosing the right account depends on your needs and financial habits. Are you a spender or a saver? Do you need easy access to your funds or are you willing to lock them away for a while? Think about your lifestyle and pick the account that best fits your financial personality.

Funding Your Financial Empire: Show Me the Money!

Once you’ve chosen your account, you’ll need to actually… you know… put money in it! You can do this in a few ways:

- Cash: Classic. Just walk into a branch and hand over the green stuff. Try not to look too suspicious when you're counting out a stack of crumpled bills.

- Check: Write a check from another account and deposit it. Just be aware that it might take a few days to clear.

- Electronic Transfer: Link your new Citibank account to an existing account at another bank and transfer funds electronically. This is usually the easiest and fastest option.

Minimum Deposit: Some accounts require a minimum initial deposit to open. Check the fine print to make sure you have enough moolah on hand.

The Grand Finale: Applying and Opening Your Account

You have two options here: apply online or head to a physical branch. Online is generally faster and more convenient, but if you prefer the human touch (or you just want to grill a banker about the nuances of interest rates), a branch visit is the way to go.

During the application process, be prepared to answer some questions about yourself. They’ll want to know your employment status, income, and other financial details. Don’t worry, they’re not judging you (probably). They just need to assess your risk profile.

Once your application is approved, congratulations! You’re officially a Citibank customer! You'll receive your account details, debit card (eventually), and access to online banking. Now you can start managing your money like a pro… or at least, like someone who knows what they're doing (most of the time).

So there you have it! Opening a bank account at Citibank isn't as scary as it seems. Just gather your documents, choose your account wisely, and prepare to answer a few questions. And remember, if all else fails, blame it on the dog.