What Credit Score Can Buy A House

Okay, let's talk houses. Dreamy, right? But before you start picking out paint colors and arguing about whether or not you really need that avocado-shaped pool float, there's a little hurdle called a credit score.

Think of your credit score like your financial popularity rating. It's a three-digit number that tells lenders how likely you are to pay back the money they lend you. The higher the number, the more lenders will swoon. But what number do you actually need to snag those house keys?

The Credit Score Sweet Spot: Not as Scary as You Think!

Good news! You don't need a perfect 850 credit score to buy a house. You also don't need to be a millionaire or come from old money. While a higher credit score definitely opens doors to better interest rates, it’s not the only thing that matters.

Must Read

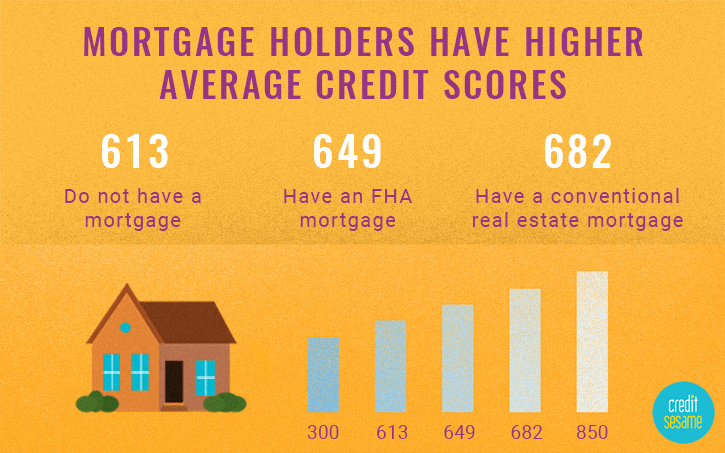

So, what's the magic number? Well, it’s more like a range. Generally, you'll want to aim for a score of 620 or higher to qualify for a conventional mortgage. Think of it like needing a C- in a very important class – not amazing, but definitely passing! But before you assume that a 620 is all you need, take a look at the big picture.

Is 620 the absolute minimum? Unfortunately, yes, for most conventional loans. But lenders also consider other factors, like your debt-to-income ratio (how much you owe compared to how much you earn), your down payment, and your employment history. These factors act as mitigating factors that affect your qualification.

The FHA Option: A Little More Forgiving

If your credit score is a little… shall we say, "under construction," don’t despair! There's another option called an FHA loan. FHA loans are backed by the Federal Housing Administration, and they're often more lenient with credit score requirements. You could get approved with a score as low as 500, but you'll likely need a larger down payment.

Think of it like this: a lower credit score is like showing up to a party with a slightly questionable outfit. You might still get in, but you might need to bring a really awesome gift (aka, a bigger down payment) to sweeten the deal.

Why a Good Credit Score Matters (Even If You Can Buy With Less)

Okay, so you can potentially buy a house with a lower credit score. But should you? A higher credit score isn't just about getting approved; it's about getting the best possible interest rate. And trust me, that can save you thousands of dollars over the life of your loan.

Imagine two people buying the same house. One has a stellar credit score and gets a 6% interest rate. The other has a so-so score and gets a 7% rate. That extra 1% might not seem like much, but over 30 years, it could mean the difference between a vacation home and ramen noodles for dinner every night. So, paying a little extra on your credit cards now might be worth a tropical vacation!

Boosting Your Score: It's Like Leveling Up in a Video Game

Feeling like your credit score needs a boost? Don't worry, it's not set in stone! Here are a few simple ways to level up your financial game:

- Pay your bills on time, every time. This is the biggest factor affecting your credit score.

- Keep your credit card balances low. Aim to use less than 30% of your available credit.

- Check your credit report for errors. Mistakes happen! Dispute anything that's inaccurate.

- Become an authorized user on someone else's credit card. If they have good credit habits, it can help boost yours. (Just make sure they're responsible!)

The Takeaway: It's a Journey, Not a Destination

Buying a house is a big deal, and your credit score is just one piece of the puzzle. Don't get discouraged if your score isn't perfect right now. Focus on improving your financial habits, and you'll be well on your way to homeownership. Remember, it's not about getting the perfect score, it's about getting a score that allows you to achieve your dreams. And who knows, maybe you will get that avocado-shaped pool float after all!