The Factor Used Most Often When Underwriting

So, I was grabbing a latte the other day (extra foam, don't judge!), and this whole underwriting thing came up. Turns out, my friend, Mark, thinks it's some super-complicated wizardry involving actuarial tables and sacrificing goats to the risk gods. Okay, maybe not the goats. But close!

Well, I told him, it's not that crazy. There's one factor that rises above the rest, the king of the hill, the ultimate decider when those underwriting wizards (okay, underwriters) are sizing you up. And guess what it is?

It's not your charm. (Sorry, Mark.)

Must Read

It's not your uncanny ability to predict the weather using only your left knee. (Impressive, but irrelevant.)

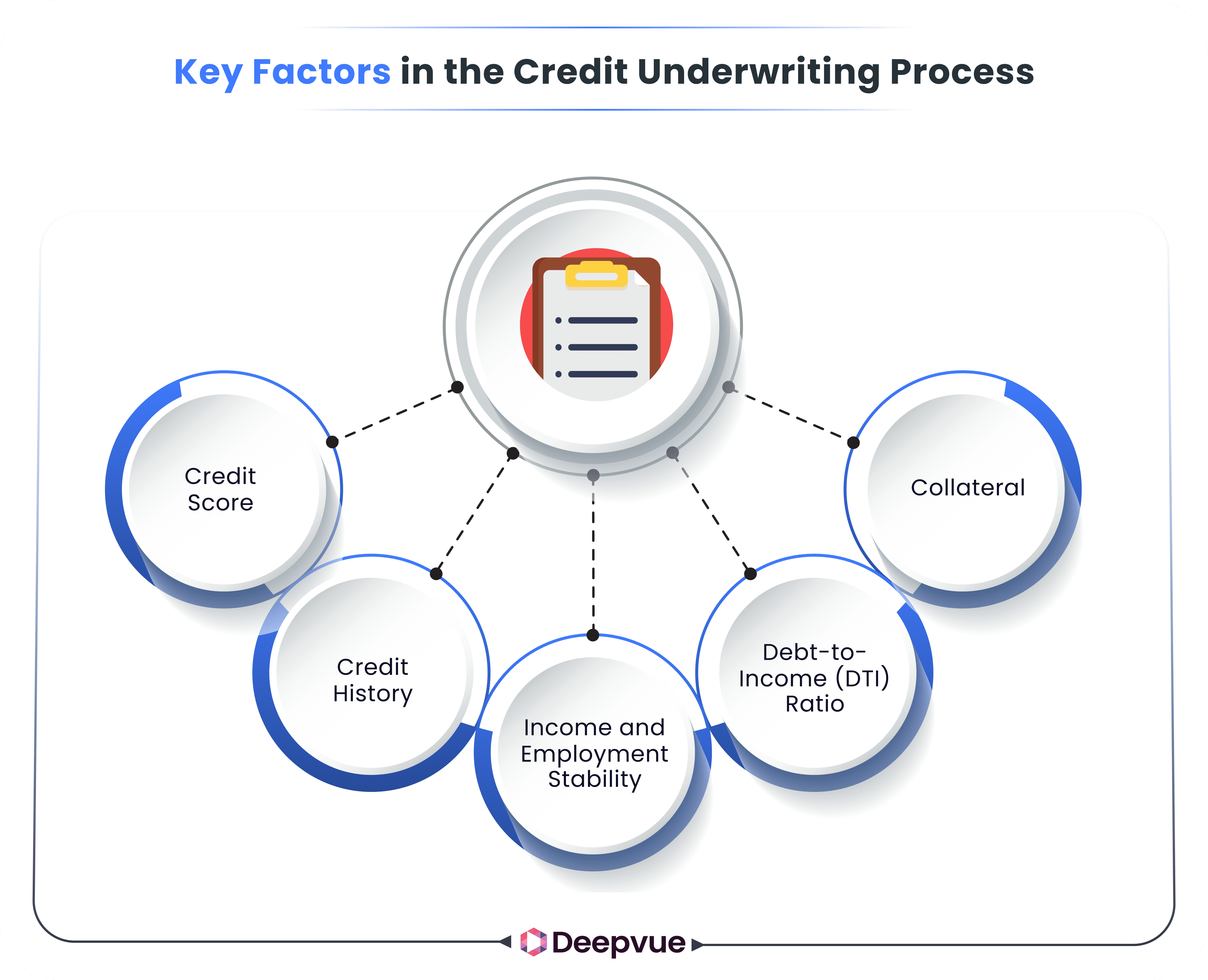

Drumroll, please… it's your credit score!

Why Credit Scores Reign Supreme

Yep, that three-digit number that can make or break your financial dreams. Seems simple, right? But the power it wields! I tell you, it’s like the financial equivalent of the One Ring from Lord of the Rings. Except instead of controlling Middle-earth, it controls your ability to buy a house, get a car loan, or even land that sweet apartment with the rooftop pool (dreams!).

Think about it. What is underwriting really? It's basically someone (or some algorithm, because hello, automation!) trying to figure out how likely you are to pay back money you borrow. And what's a quick and dirty way to assess that likelihood? You guessed it: your past performance with paying back… other money. Hence, the credit score.

Lenders and insurers see your credit score as a crystal ball into your financial future. A high score whispers sweet nothings of responsible repayment and fiscal stability. A low score, well, it screams of missed payments, defaulted loans, and a general disregard for financial obligations. It’s a bit harsh, I know. Life happens!

Beyond the Numbers: What Else Matters? (A Little)

Now, before you hyperventilate and start meticulously checking your credit report every five minutes (we've all been there!), it's worth noting that other factors do play a role. Just not as big of a role as your credit score. They’re like the backup dancers to your credit score's lead singer. Supportive, but not the main attraction.

For example, your income is definitely important. You can have a perfect credit score, but if you’re only earning enough to buy ramen noodles (every day!), a lender might hesitate to give you a massive mortgage. They need to be reasonably sure you can actually afford to repay the loan.

Then there’s your debt-to-income ratio (DTI). This is basically how much of your monthly income is already going towards debt payments. The lower the better! High DTI means you're already stretched thin, making it riskier for you to take on even more debt.

Your employment history matters too. A stable job shows you have a consistent source of income. Jumping from job to job every few months might raise some red flags.

And finally, the type of asset you're trying to insure or borrow against. Underwriting a mortgage is different than underwriting a car loan. Each has its own specific risks and considerations.

The Moral of the Story: Treat Your Credit Score Like Gold

So, next time you’re out there in the financial wild, remember: your credit score is your best friend. Treat it well! Pay your bills on time (seriously, always on time). Keep your credit utilization low (don’t max out those credit cards!). And check your credit report regularly for any errors. You wouldn’t let a typo ruin your novel, would you? Don't let a mistake mess with your financial future either!

Think of it this way: building good credit is like leveling up in a video game. Each positive action (paying bills on time, etc.) adds experience points, boosting your score and unlocking new levels of financial freedom. Who doesn't love leveling up?

Now, if you'll excuse me, I need to go check my credit score. Just kidding! (Maybe.) But seriously, take care of that credit score, and it will take care of you. And maybe, just maybe, you'll finally get that rooftop pool apartment. Now that's a happy ending!