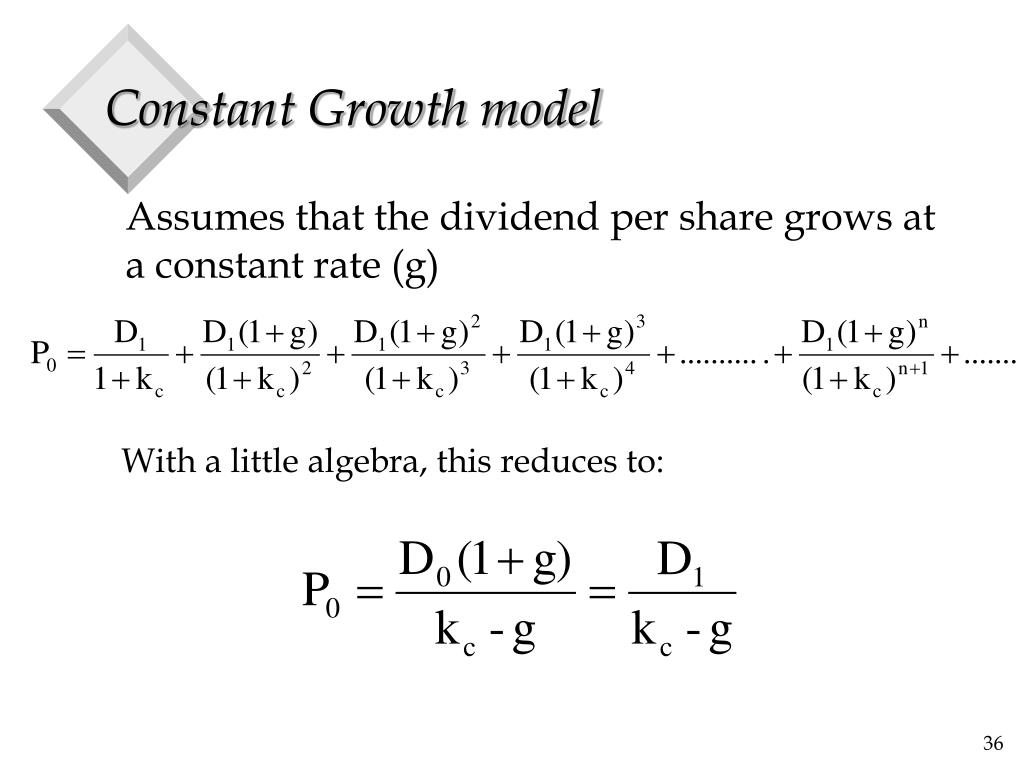

The Constant Growth Model Assumes That

Okay, so picture this: you're at a café, right? Latte in hand, eyeing that suspiciously delicious-looking pastry. And your friend leans in and says, "Hey, wanna talk about the Constant Growth Model?" You'd probably choke on your foam art. But stick with me, it's not as terrifying as it sounds. Especially when we dissect its, shall we say, bold assumptions.

The Constant Growth Model, or Gordon Growth Model (named after Myron J. Gordon, not the celebrity chef, sadly), is a way to figure out what a stock is worth. It's all about dividends, those sweet, sweet payouts companies give to shareholders. The basic idea is that a stock's value is based on the present value of all its future dividends. Makes sense, right? Like finding the value of that chocolate croissant by estimating how many delicious bites you'll get from it.

Assumption #1: Dividends Grow at a Constant Rate…Forever!

Here's where the fun – and the potential for epic fails – begins. The first and most infamous assumption is that the company's dividends will grow at a constant rate. Forever. Yes, FOREVER. Imagine trying to convince your grandma that she will bake cookies at exactly 5% more than the previous year, until the end of time. Good luck with that!

Must Read

Seriously, think about it. Can anything grow at the same rate forever? Not even weeds in my garden manage that kind of consistent performance. Economies have their ups and downs. Companies face competition, innovation, and the occasional scandal involving questionable accounting practices. Projecting a static rate into the infinite future is, well, ambitious. Borderline delusional, even. But hey, nobody ever got rich by being underconfident (maybe?).

Think about Amazon. They didn't even pay a dividend for years, instead investing every penny they earned. What if someone had tried to use this model on them in their early days? The result would have been as accurate as a weather forecast for the year 2342. Spoiler alert: flying cars will probably be involved!

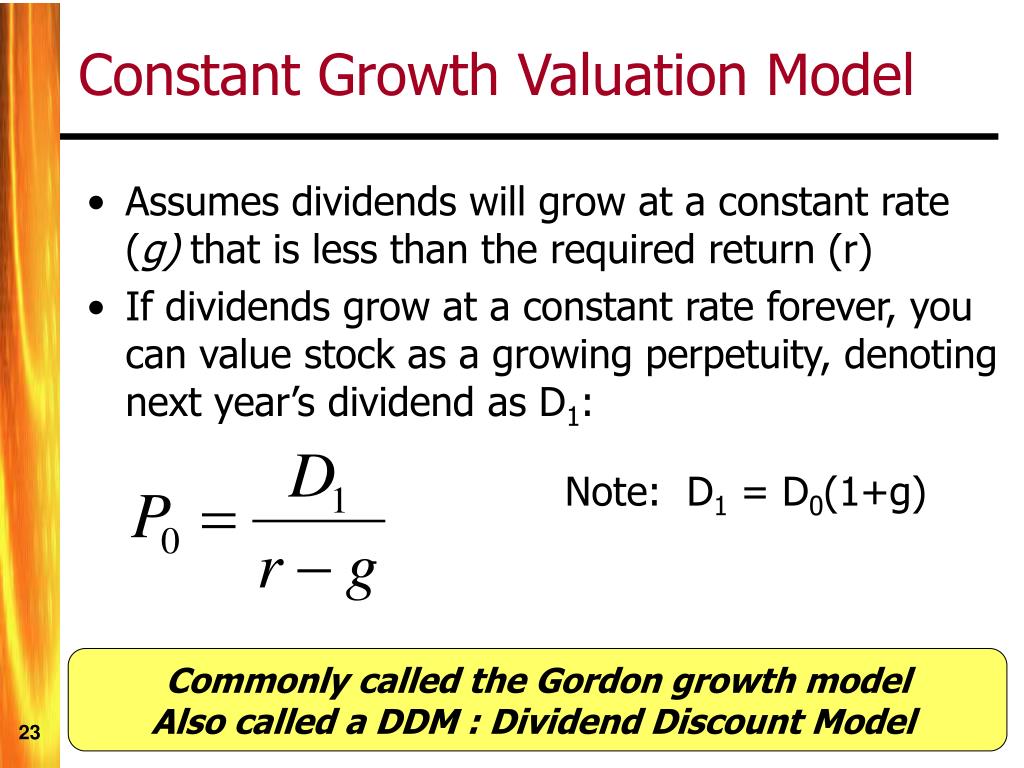

Assumption #2: The Growth Rate is Less Than the Required Rate of Return

The second whopper of an assumption is that the constant dividend growth rate (that "g" in the formula) has to be less than your required rate of return (that "r" in the formula). Why? Because if "g" is higher than "r," the model goes haywire. Like a self-driving car suddenly deciding it wants to explore the local petting zoo. The output is meaningless, and you might end up owing somebody money for the privilege of using the model.

Essentially, this assumes that your investment shouldn’t require more return than the company’s growth. Think of it as the company working for you. If your requirements become too great, the value can become infinite (or some other nonsense number), which, as any economist will tell you, is highly unlikely. Especially in the context of the stock market.

It's like saying the price of a single croissant must always be lower than the national debt. Okay, maybe not that extreme, but you get the idea.

Assumption #3: Stable Dividend Policy

The third major assumption is that the company maintains a fairly stable dividend policy. Meaning they aren't likely to suddenly slash dividends to fund a new venture involving artisanal cheese or robot butlers. Companies that consistently pay and gradually increase dividends are better candidates for this model.

Imagine a company that’s flip-flopping more than a politician in an election year. One year, they pay out a huge dividend, the next year, they hoard all the cash. The Constant Growth Model would throw its hands up in despair. It craves predictability, stability, and the gentle rhythm of ever-increasing payouts.

So, Is It Totally Useless?

Not necessarily! Despite these somewhat ludicrous assumptions, the Constant Growth Model can be a useful starting point. It's a tool, not a crystal ball. Think of it as a rusty wrench in a toolbox filled with complex algorithms and AI-powered analytics. It's simple, easy to use, and sometimes, just sometimes, it gets the job done.

It works best for mature, stable companies with a track record of consistent dividend growth, think utility companies or those selling everyday consumer products (think: toilet paper and coffee). Companies that are less like rockstars and more like reliable librarians.

Just remember to take the results with a grain of salt (or a generous dollop of whipped cream on that pastry). And always, always do your own research. Don't rely solely on a model that assumes dividends grow forever! After all, even the most delicious croissant eventually gets eaten.

Now, if you'll excuse me, I see a chocolate pastry calling my name, whose value, if estimated using this model, would be significantly affected by my subjective growth rate of enjoyment.