Is 552 A Bad Credit Score

Okay, so picture this: you're at a cafe, right? Sipping on your latte (extra foam, naturally), and your friend leans in conspiratorially. "Dude," they whisper, "My credit score...it's like, 552. Am I doomed to a life of ramen and borrowing my neighbor's Netflix password?"

Well, hold on to your oat milk, my friend. Let's unpack this 552 business. Is it good? Nah. Is it apocalyptic? Probably not. Think of your credit score like your dating profile. 552 isn't going to land you a supermodel, but it doesn't mean you're destined to be single forever either. You just gotta work on it a bit.

The Cold, Hard Truth About 552

Let's be blunt: a 552 credit score falls squarely into the "poor" or "bad" category. Ouch. Think of the FICO score range, which is the most popular, as a kind of social hierarchy. 300 is basically credit Siberia (good luck getting a library card, let alone a mortgage!), and 850 is like being crowned King or Queen of Creditlandia.

Must Read

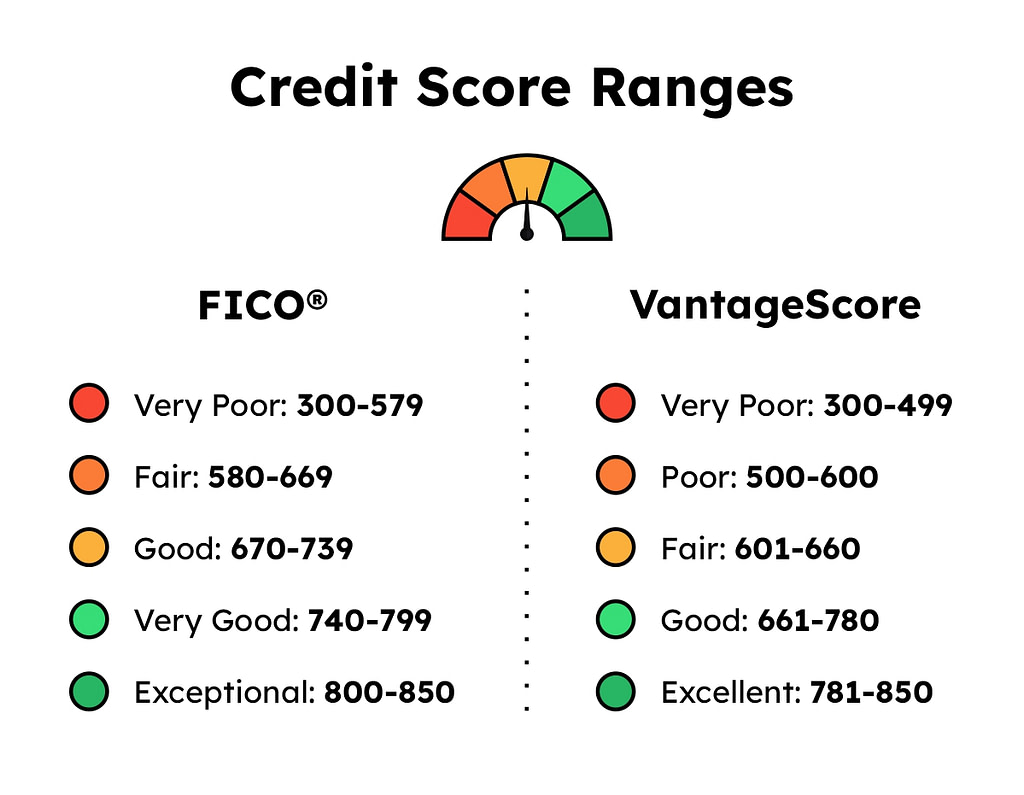

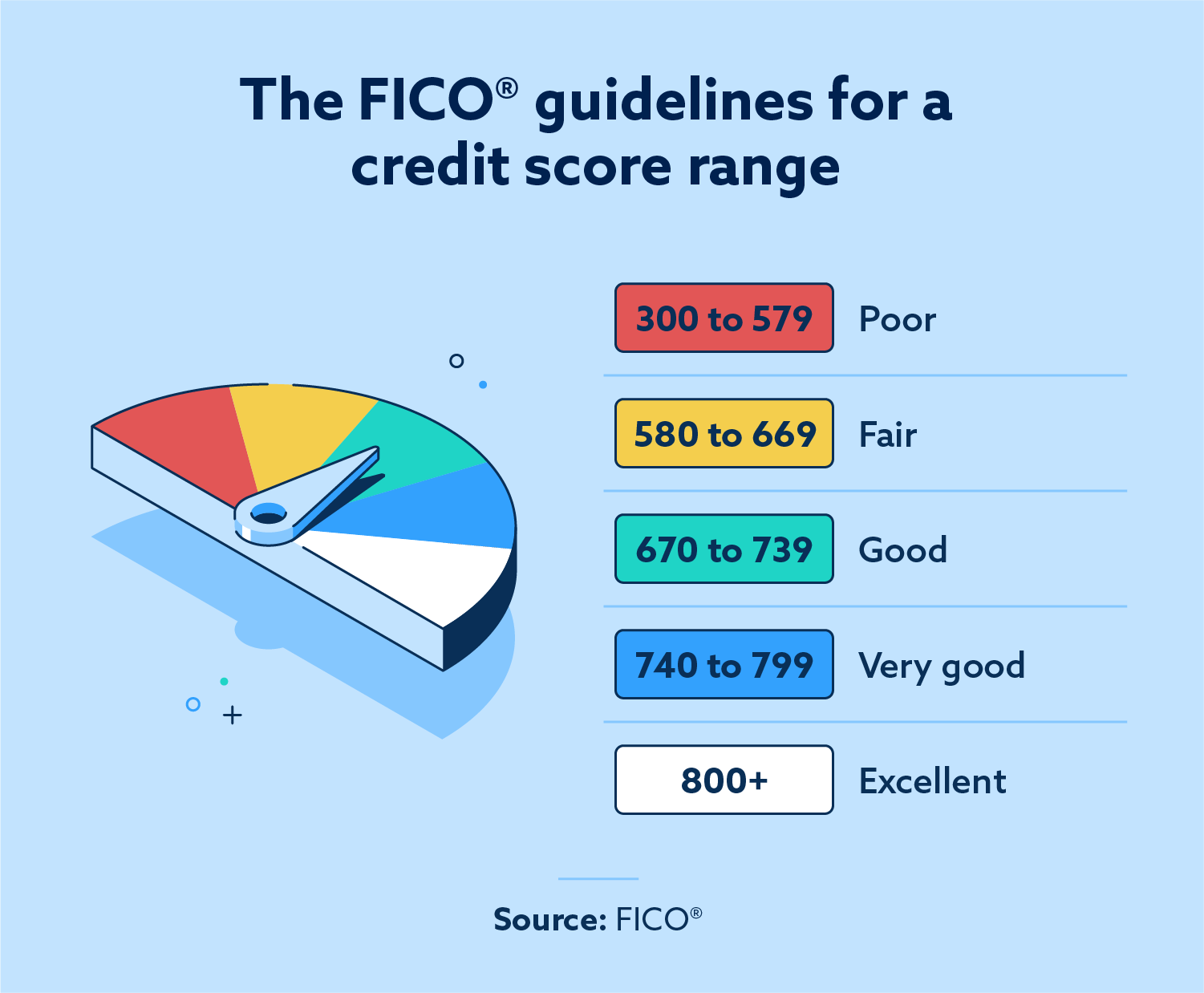

Here's the breakdown (roughly):

- 300-579: Very Poor (Ramen diet incoming!)

- 580-669: Fair (Okay, maybe slightly fancier ramen.)

- 670-739: Good (Now we're talking! Maybe afford a side of guac?)

- 740-799: Very Good (Hello, travel rewards!)

- 800-850: Exceptional (You're basically a credit unicorn.)

So, yeah, 552 isn't exactly setting off fireworks. It means you've probably had some credit hiccups along the way. Maybe a missed payment here, a maxed-out credit card there...we've all been there (okay, maybe not all of us, but you get the idea).

Here's a surprising fact: Did you know that some employers actually check your credit score before hiring you? I know, right? Talk about judging a book by its cover (or, in this case, your history of paying bills on time).

What 552 Means for You (Besides Ramen)

Having a credit score of 552 can make life a bit…challenging. Here’s a taste of what you might encounter:

* Higher interest rates: Banks will see you as a risky borrower, so they'll charge you more to borrow money. Think of it as a "bad credit tax." On everything. * Difficulty getting approved for loans: Car loans, mortgages, personal loans...they might be tough to snag. You might be forced to rely on less-than-ideal lenders with, shall we say, predatory interest rates. * Trouble renting an apartment: Landlords often check credit scores to see if you're a responsible tenant. A 552 might make them hesitant to hand over the keys. * Higher insurance premiums: Believe it or not, your credit score can impact your insurance rates. Apparently, people with lower scores are statistically more likely to file claims. Go figure. * That "declined" feeling: You know, when you apply for something and get that dreaded email? Yeah, you might see a lot of those.Basically, it's like trying to navigate life with lead boots on. Every financial step feels a little harder.

But Don't Despair! There's Hope! (and Maybe a Little Credit Counseling)

Okay, okay, I've painted a pretty grim picture. But fear not! A 552 isn't a life sentence. You can improve your credit score. It takes time, patience, and a willingness to make some changes, but it's totally doable.

Think of it as a credit score glow-up! Here are some strategies:

A little joke for you: What did the credit score say to the borrower? "Don't worry, I'll bounce back!"

Another Surprising Fact: Did you know you are entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year? Go to AnnualCreditReport.com. No excuses!

So, is 552 a bad credit score? Yeah, it's not ideal. But it's not the end of the world. With a little effort, you can turn that 552 into a number you're proud of. And who knows, maybe someday you'll be the one dispensing credit advice at the café, latte in hand.