In A Purely Competitive Industry Each Firm

Imagine a world overflowing with lemonade stands! Every kid on the block, Grandma, even Mr. Grumbles from next door, is selling lemonade.

That, my friends, is a bit like a purely competitive industry. It's all about lots and lots of sellers offering pretty much the same thing.

Lemonade Stand Economics

Think about it: is Mr. Grumbles going to get away with charging $10 a glass when Susie down the street is selling hers for 50 cents? Absolutely not!

Must Read

In this kind of market, each lemonade entrepreneur, each firm, is a price taker. They don't get to decide the price; the market does.

No Price Power Here!

The market price is determined by everyone collectively – all the buyers and all the sellers shouting out their offers.

Each individual lemonade seller is so tiny compared to the whole market that trying to charge even a penny more would send all their thirsty customers running to the competition.

They simply have to accept the going rate, or watch their lemonade go sour.

Identical Products, Identical Problems (and Opportunities!)

Another key thing about our lemonade stand scenario (and purely competitive industries in general) is that everyone's lemonade is essentially the same.

No secret family recipe that magically turns into liquid gold! Just good old H2O, lemons, and sugar.

This is known as homogenous products. Because the product is the same, there's no advantage in charging more.

A Level Playing Field (Sort Of)

Since everyone's lemonade is equally refreshing, customers will flock to whoever offers the best deal.

This creates intense competition, which drives down profits. Each seller must be as efficient as possible.

There's no room for fancy decorations or hiring celebrity spokespersons (unless you find a very thirsty local squirrel willing to work for nuts!).

Easy Entry, Easy Exit

So, what happens if you see all these lemonade stands raking in the dough (hypothetically, of course)?

You might think, "Hey, I can make lemonade too!" And guess what? You probably can!

Purely competitive industries usually have low barriers to entry. It's easy for new firms to jump in and start selling.

Come One, Come All!

This easy entry is a double-edged sword. It means more competition, which can drive prices down even further.

But it also means that if you're losing money, you can easily pack up your lemons and go home. There are low barriers to exit, too!

No complicated contracts or massive investments holding you back. Freedom!

Perfect Information for Everyone!

In our super-simplified lemonade stand world, everyone knows everything. Customers know the price and quality of lemonade at every stand.

Sellers know the costs of lemons, sugar, and cups. This is known as perfect information. No secrets here!

Everyone is on the same page, making rational decisions based on complete knowledge.

The Reality Check

Okay, okay, so a real-world lemonade stand market is probably not perfectly competitive. Little Timmy's lemonade might actually be a secret family recipe!

But the lemonade stand analogy gives you a good idea of the key characteristics of a purely competitive market: many sellers, identical products, easy entry and exit, and perfect information (in theory!).

Think about agricultural products like wheat or corn. There are tons of farmers, the products are pretty similar, and it's relatively easy to start or stop farming (though it still requires hard work and investment!).

The Firm's Perspective

So, what does all this mean for each individual firm operating in a purely competitive market?

Well, as we already discussed, each firm is a price taker. They have to accept the market price.

They can sell as much as they want at that price, but they can't sell anything if they try to charge more.

The Demand Curve of a Price Taker

This means that the demand curve facing each individual firm is perfectly elastic – a flat line at the market price.

Imagine drawing a graph with price on the vertical axis and quantity on the horizontal axis. The firm's demand curve would be a straight, horizontal line.

This illustrates that a single firm can sell as many glasses of lemonade as they want, up to their production capacity, at the prevailing market price, but nothing at even one cent higher.

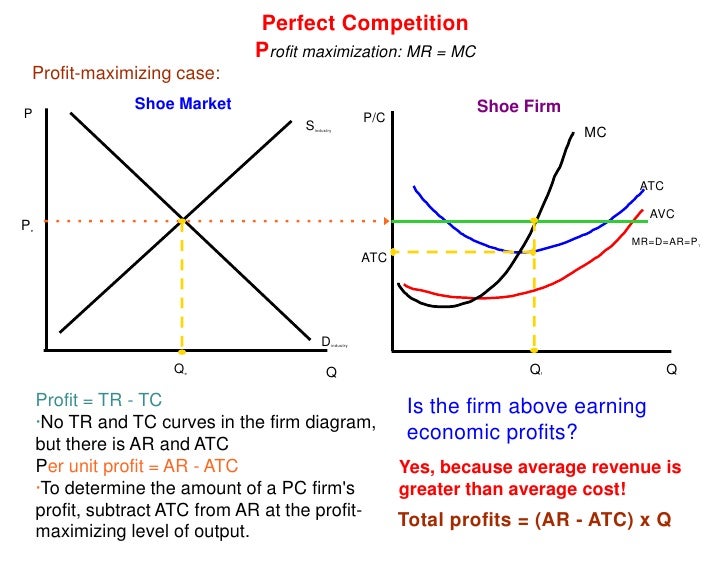

Maximizing Profits in a Competitive World

Even though they can't control the price, firms in a purely competitive market still want to maximize their profits.

They do this by carefully managing their costs and choosing the optimal level of output.

They want to produce where their marginal cost (the cost of producing one more unit) equals the market price.

Marginal Cost Meets Market Price

Why marginal cost equals market price? Because if the marginal cost is less than the market price, that means they can make more profit by producing one more unit.

If the marginal cost is greater than the market price, that means they're losing money on each additional unit they produce, so they should cut back.

The sweet spot is where marginal cost and market price are equal!

Long-Run Equilibrium

In the long run, something interesting happens in purely competitive markets. If firms are making profits, new firms will enter the market, driving down prices.

If firms are losing money, some will exit the market, driving prices up.

This process continues until firms are earning only a normal profit – just enough to cover their costs and stay in business.

The Zero-Profit Condition

This is known as the zero-profit condition. It doesn't mean that firms aren't making any money at all!

It just means that they're earning enough to cover their opportunity cost – the return they could get by investing their resources elsewhere.

It is called economic profit zero, not accounting profit!

The Benefits of Pure Competition

While it might sound tough for individual firms, purely competitive markets are actually great for consumers.

Because of intense competition, prices are driven down to the lowest possible level. You get your lemonade for a steal!

Resources are allocated efficiently, and there's no room for waste or inefficiency. It's a win-win!

A Word of Caution

Of course, perfectly competitive markets are rare in the real world. Most industries have at least some degree of imperfect competition.

But understanding the principles of pure competition is a helpful starting point for analyzing how markets work and how firms behave.

So next time you're enjoying a refreshing glass of lemonade, remember the lessons of the lemonade stand and the wonders of pure competition!