Identify A True Statement About The Effective Annual Rate

Okay, folks, let's talk about something that sounds intimidating but is actually super useful: the Effective Annual Rate (EAR). Think of it as the financial version of decoding a secret menu item at your favorite burger joint. It's all about getting the real deal, the true cost, and not being fooled by fancy marketing terms.

Why Should I Even Care?

Imagine you're at a farmer's market. One stall offers a "special deal" on strawberries: 10% off! Sounds great, right? But what if they only give you the discount if you buy strawberries every single week for the next year? Suddenly, that "special deal" feels a little less…special. That's where EAR comes in! It helps you see the actual cost or return, especially when interest is compounded more than once a year.

Think of it this way: Would you rather know how much your car loan REALLY costs you each year, or just a fraction of the cost spread out over monthly payments that conveniently hide the bigger picture? Exactly! EAR gives you the bigger picture.

Must Read

So, What's the True Statement About EAR?

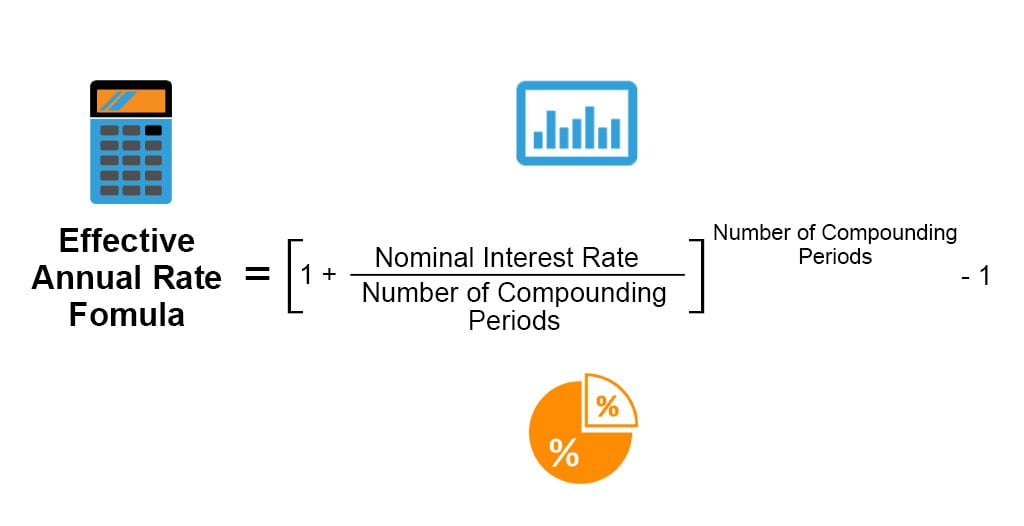

Here's the key: The Effective Annual Rate is almost always HIGHER than the stated, or nominal, interest rate when interest is compounded more than once a year. Let's break that down:

- Nominal Interest Rate: This is the advertised rate. The "fancy" one. The one that might lure you in. It's the 10% off strawberries!

- Compounding: This is how often interest is added to your principal (the original amount you borrowed or invested). Could be monthly, quarterly, daily...even continuously!

- Effective Annual Rate: This is the real annual rate you're paying or earning, after taking compounding into account. The actual price of those strawberries over the year!

Why is EAR higher? Because with each compounding period, you're earning (or paying) interest on a slightly larger amount. It's like a snowball rolling downhill – it gets bigger and bigger as it goes! That compounding effect adds up!

Examples From Everyday Life (Because Finance Shouldn't Be Scary!)

Scenario 1: Savings Account

Let's say you have a savings account that offers a nominal interest rate of 5% compounded monthly. That sounds pretty good, right? Well, the EAR will actually be a bit higher than 5% because the interest is added to your account balance every month, and then you earn interest on that new, slightly larger balance the next month. It's a tiny difference month-to-month, but over a year, it adds up. You're essentially earning interest on your interest!

:max_bytes(150000):strip_icc()/compoundinterest_final-5c67da5662ba458f8d9d229ab4ca4292.png)

Scenario 2: Credit Card

Uh oh! That credit card with a "low" 18% APR? That's the nominal rate. Because credit card interest is usually compounded daily (yikes!), the EAR is going to be significantly higher than 18%. This is why making even small payments is so important – you're not just paying down the principal, you're also minimizing the impact of that compounded interest.

The Takeaway: Don't Be Fooled!

The bottom line? Always look at the EAR, not just the nominal interest rate. It’s the true cost or true return. It's like choosing between a generic soda and a premium one – both quench your thirst, but one gives you a better experience for the same cost. By understanding EAR, you can make informed financial decisions, whether you're choosing a savings account, a loan, or a credit card.

Remember, knowledge is power (and saves you money!) So, next time you see an interest rate, dig a little deeper and find that EAR. Your wallet will thank you!

One Last Thought: The more frequently the interest is compounded, the higher the EAR will be compared to the nominal rate. Keep that in mind!