How Long Is A Statement Cycle

Ever felt like your bills just appear out of nowhere? Or wondered exactly when your credit card interest starts kicking in? Well, understanding your "statement cycle" is like finding a secret map to your financial world! It might sound a bit technical, but trust me, it’s one of the simplest and most powerful tools you can master for smoother money management. Far from being a dry accounting term, knowing your statement cycle can actually bring a surprising amount of clarity and control to your everyday finances, making it a truly useful piece of knowledge for everyone.

For beginners in personal finance, grasping the statement cycle is absolutely fundamental. It helps you know exactly when your spending period ends and when your payment is due, preventing those dreaded late fees and helping you avoid unnecessary interest charges. For families, it's a budgeting superpower. You can align your household expenses, plan bigger purchases more strategically, and ensure everyone's on the same page regarding bill payments. Even for the casual everyday reader, knowing your cycle means smarter spending, clearer budgeting, and significantly less financial stress. It’s all about taking control and making your money work for you, not against you.

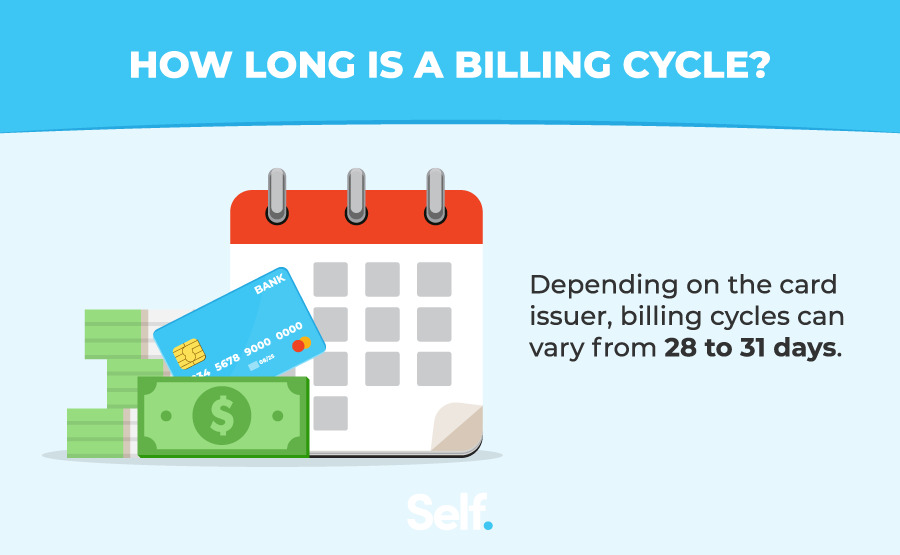

So, how long is a statement cycle? For most credit cards and bank accounts, it’s typically around 28 to 31 days – roughly one month. This period starts on one specific date and ends on another, after which your statement is generated. For example, if your cycle starts on the 5th of July, it will likely end around the 4th of August. The balance from this period then becomes your minimum payment or full balance due. Importantly, your payment due date is usually about 21-25 days after your statement cycle ends. This grace period is key, as it gives you time to pay without incurring interest on new purchases (if you pay your full statement balance). While most major financial products stick to this monthly rhythm, some utilities might have slightly different cycles, perhaps bi-monthly, but the core idea of a defined billing period remains consistent.

Must Read

Ready to become a statement cycle guru? Here are some simple, practical tips for getting started:

- Find It: Look at your latest credit card or bank statement. You'll usually see "Statement Period," "Billing Cycle," or "Activity Period" clearly listed with a start and end date.

- Mark Your Calendar: Add your cycle end date and payment due date to your calendar or phone reminders. This helps you visualize your spending window and plan ahead.

- Plan Purchases: Need to make a big purchase? If you can pay it off quickly, timing it for the start of a new cycle gives you nearly two months before the payment is due (assuming you pay your full statement balance during the grace period!).

- Automate Smartly: Auto-pay is great for convenience, but still review your statement each month to check for errors and understand your spending patterns.

- Interest Awareness: Remember, if you carry a balance on a credit card, interest generally starts accruing after the due date of your previous statement's balance, not just on new purchases. Knowing your cycle helps you understand this better.

See? Understanding "how long is a statement cycle" isn't just about dry numbers; it's about gaining genuine power over your finances. It's a simple piece of knowledge that can help you avoid fees, budget more effectively, and feel much more confident about your money situation. It’s time to unlock this easy secret and enjoy the peace of mind that comes with being financially savvy!