Does Cosigning Affect Your Credit Score

So, you're thinking about cosigning? Maybe your best friend wants a car. Or your niece needs help with an apartment. It's a big decision! But before you grab that pen, let's talk about something important: your credit score. Does cosigning affect it? Buckle up, because the answer isn't always a simple "yes" or "no." It's more like a "maybe, kinda, depends!"

The Good, the Bad, and the Cosigned

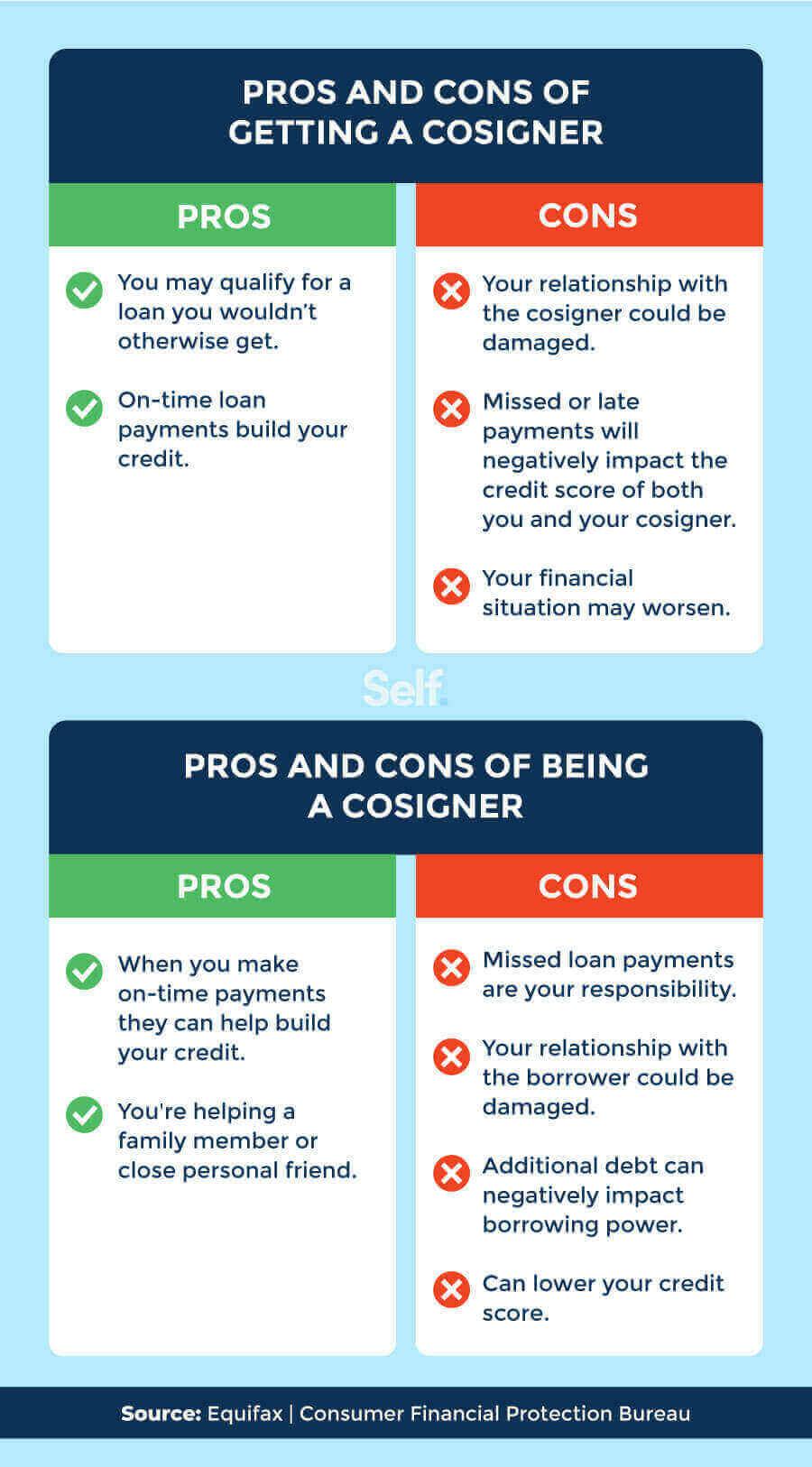

Let's get this straight. Cosigning is basically saying, "Hey, if they don't pay, I will!" You're putting your good name (and your credit) on the line. Think of it like this: you're promising to be the superhero backup in case the original borrower trips and falls. Super cool, right? Until you realize you might be doing all the heavy lifting.

The good news? Cosigning itself won't automatically ding your score. Just signing the paperwork doesn't magically make your credit take a nosedive. Phew! But here's where things get interesting.

Must Read

When Cosigning Turns Sour (and Affects Your Credit)

Imagine this: your friend, the one you cosigned for, starts missing payments. Oops! This is where the fun begins (not really). Those missed payments? They're not just hurting their credit; they're hurting yours too. Because, remember? You promised to pay if they didn't. And credit bureaus take promises seriously. Missed payments are like little credit score gremlins, nibbling away at your hard-earned good standing.

Delinquency, collections, even a default – all these nasty things can show up on your credit report because you cosigned. It's like getting a parking ticket for a car you weren't even driving! Annoying, right?

Utilization Nation: Another Credit Score Culprit

Here's another sneaky way cosigning can affect your credit. It impacts something called your credit utilization ratio. This is basically how much credit you're using compared to how much you have available. Lenders love to see a low utilization ratio (generally below 30%).

When you cosign a loan, that loan can show up on your credit report as your debt. Even though you're not actually the one making the payments (hopefully!), it still looks like you owe that money. This can increase your credit utilization ratio and potentially lower your score. Imagine trying to bake a cake with too much flour – things just get messy!

The Cosigning Silver Lining (If There Is One)

Okay, it's not all doom and gloom. There's a tiny chance cosigning could help your credit. If the primary borrower makes all their payments on time, every time, that can look good. It shows responsible borrowing and repayment, and sometimes that can have a slight positive effect. Think of it like getting a gold star for being a really, really good backup. But honestly, the risks usually outweigh the potential rewards.

Before You Cosign: A Little Self-Care

So, what's the takeaway? Cosigning is a big deal! Before you agree to it, ask yourself these questions:

- Can I really afford to pay this loan if the primary borrower defaults?

- Do I completely trust this person to be responsible with their finances?

- Am I willing to potentially sacrifice my own credit score for them?

If you answered "no" to any of those questions, it's probably best to politely decline. It's okay to say no! Your credit score (and your financial well-being) is important. Remember, good fences make good neighbors. And in this case, a good "no" can save you a lot of heartache (and credit score damage).

Think of cosigning like lending someone your favorite sweater. You hope they'll take care of it, but there's always a chance they'll spill coffee on it or, worse, never give it back! Your credit is way more valuable than a sweater. Protect it!

And hey, if you're curious about your own credit score, why not check it out? Knowledge is power! And knowing your score is the first step to keeping it in tip-top shape. After all, it's your financial superpower. Use it wisely!

Cosigning a loan is a serious financial commitment that could have a big impact on your credit.

So there you have it. Cosigning: a thrilling (and potentially terrifying) adventure in the world of credit. Choose wisely, friends! And remember, your credit score will thank you.