Difference Between Variable And Fixed Rate

Hey, so you're trying to figure out the whole variable vs. fixed rate thing? It's like choosing between that predictable vanilla ice cream (yawn, maybe?) or a spicy mystery flavor that could be amazing... or a total disaster. Let's dive in!

Basically, it all boils down to how your interest rate behaves. And let’s be honest, interest rates are already confusing enough, right? Like, what even is LIBOR anyway? (Don’t worry, we won't go there).

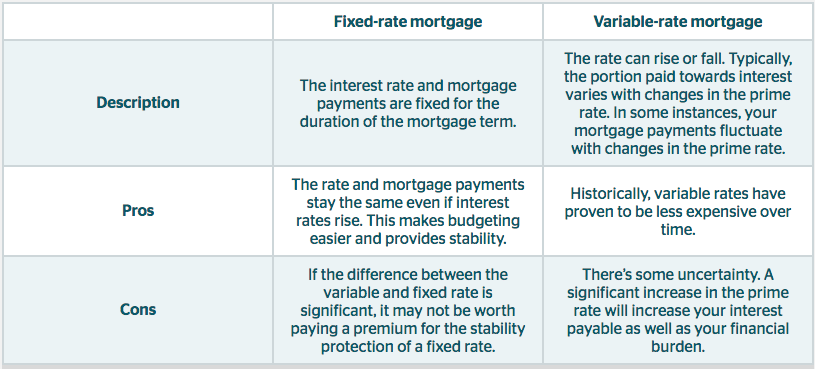

Fixed Rate: Predictable, Like Your Grandma's Cooking

Think of a fixed rate as the dependable friend who always shows up on time. It stays the same for the entire loan term. Yep, you heard that right. No surprises! You know exactly what you'll be paying each month. Pretty sweet, huh?

Must Read

Pros:

- Predictability: Like knowing exactly how much sugar is in your coffee. No unexpected bitter sips!

- Budgeting Bliss: Makes budgeting a breeze because your payments are consistent. Finally, a budget you might actually stick to!

- Peace of Mind: Especially when interest rates are on the rise. You can smugly sip your coffee while everyone else panics. (Okay, maybe don’t actually be smug).

Cons:

- Potentially Higher Initial Rate: You might pay a bit more upfront for that sweet, sweet predictability. It's like paying extra for insurance against future interest rate hikes.

- Missed Opportunities: If interest rates fall, you're stuck with your higher rate. Ouch. FOMO is real, even with mortgages!

Variable Rate: A Rollercoaster Ride (Hold On Tight!)

A variable rate is the wild child of the interest rate world. It fluctuates with the market. It’s often tied to a benchmark rate (like the Prime Rate) plus a margin. So, when the benchmark goes up, your rate goes up. And vice versa. It's a rollercoaster of potential savings and potential… uh… financial discomfort.

Pros:

- Lower Initial Rate: Usually starts lower than a fixed rate. Yay, savings! But remember, initial savings aren't everything.

- Potential Savings: If interest rates go down (or stay low), you could save a bundle! Think of all the extra guacamole you could buy.

Cons:

- Unpredictability: Your payments can change – sometimes frequently. This can make budgeting tricky and stressful. Are you feeling lucky?

- Rate Hikes: Interest rates could skyrocket, leaving you with unexpectedly high payments. Cue the frantic ramen noodle dinners.

- Anxiety: Constant monitoring of the market and potential rate adjustments can be… well, anxiety-inducing. Do you really want another thing to stress about?

So, Which One is Right for You?

It really depends on your risk tolerance, financial situation, and crystal ball (kidding! ... mostly). Are you comfortable with risk and believe interest rates will stay low? A variable rate might be tempting. Do you crave predictability and a good night's sleep? Fixed rate might be your jam. Consider these points:

- Your Financial Situation: Can you handle potential payment increases?

- The Length of the Loan: Shorter term? Variable might be less risky. Longer term? Fixed offers more security.

- Market Conditions: What are experts predicting about interest rates? (Though, let's be honest, even the "experts" are often wrong!)

Ultimately, the best choice is the one that allows you to sleep soundly at night. Don't be afraid to talk to a financial advisor or mortgage broker to get personalized advice. They can help you weigh the pros and cons and find the best option for your unique situation. And hey, maybe bring them coffee. They deserve it!

Good luck navigating the wild world of interest rates! You got this!