Citibank Mortgage Relationship Discount

Okay, picture this: I'm knee-deep in paperwork, trying to decipher the hieroglyphics that is a mortgage application. My head's spinning. Then, like a beacon of hope (or maybe just caffeine-induced delusion), I stumble across this little phrase: "Relationship Discount." Relationship? Are we talking flowers and chocolates here, Citibank? Turns out, it's a bit more…financial.

So, let's dive into the murky waters of the Citibank Mortgage Relationship Discount. What is it? Why should you care? And is it actually worth the hassle? (Spoiler alert: sometimes, yes!).

What Exactly Is This "Relationship" Anyway?

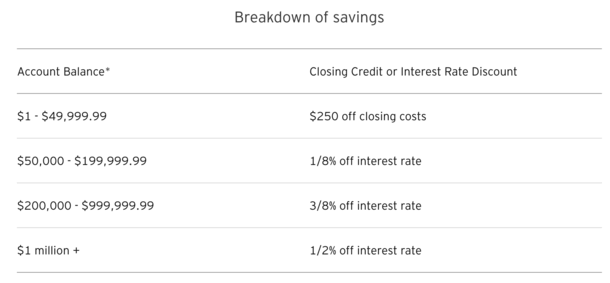

The core idea is simple: Citibank rewards customer loyalty. Basically, if you already have certain accounts with them, like a checking account, savings account, or even an investment account, you might qualify for a discount on your mortgage interest rate or closing costs. Think of it as a "thanks for sticking with us" kind of deal. Not bad, right?

Must Read

But here's the catch (there's always a catch, isn't there?): the details can get a little…dense. The size of the discount and the specific accounts that qualify vary. You'll need to dig into the fine print or, even better, actually talk to a Citibank representative. And brace yourself, because you might need a translator.

Why Should You Even Bother?

Alright, I know what you’re thinking: more paperwork, more phone calls, more confusing financial jargon. Is it really worth it? Well, consider this: even a small reduction in your interest rate can save you thousands of dollars over the life of your mortgage. We're talking serious cash here. Think of all the tacos you could buy!

A lower interest rate means lower monthly payments, which can free up your budget for other things. Or, you could pay more towards the principal each month and pay off your mortgage even faster. The possibilities are endless (well, almost).

Plus, sometimes the discount applies to closing costs, which can be a significant chunk of change upfront. So, doing a little homework could really pay off.

Okay, I'm Intrigued. How Do I Get This Magic Discount?

First, you need to be an existing Citibank customer with qualifying accounts. That’s the foundation of the relationship. Check Citibank's website or call them directly to see which accounts are eligible and what the current discount structure is. Things change, you know. Banks love to keep us on our toes.

Then, when you apply for your mortgage, make sure to ask about the relationship discount! Don't assume they'll automatically apply it. Be proactive. Be persistent. Be the person who politely hounds them until they give you all the information you need. You got this!

Also, gather your account statements. You’ll probably need to provide proof that you actually have the qualifying accounts. And, you know, be prepared for the paperwork. It’s a mortgage, after all.

The Fine Print (Because There's Always Fine Print)

Here's the thing: the Citibank Mortgage Relationship Discount isn't always the best deal out there. You need to compare it to other mortgage offers from different lenders. Don't just assume that because you're getting a "discount" with Citibank, it's automatically the cheapest option.

Get quotes from multiple lenders. Compare interest rates, fees, and terms. See what makes the most sense for your financial situation. It’s like shopping for anything else – you want to get the best bang for your buck. And, honestly, sometimes you'll find a better deal elsewhere. Don't be afraid to walk away.

And remember, the discount may be contingent on maintaining those qualifying accounts. So, if you close your checking account, you might lose your mortgage discount. Read. The. Fine. Print. Seriously.

Final Thoughts: Is It Worth It?

The Citibank Mortgage Relationship Discount can be a great way to save money on your mortgage, if you already bank with Citibank and if the discount is competitive with other offers. Do your homework, compare your options, and don't be afraid to negotiate. After all, you’re the one taking out the mortgage. You're in the driver's seat (or at least, you should be!).

And who knows, maybe you'll even develop a real "relationship" with your mortgage lender. Okay, probably not. But hey, at least you'll save some money!