Can Utility Bills Affect Your Credit

Hey friend! Ever wonder if those pesky utility bills – you know, the ones that seem to magically appear in your inbox every month – can actually mess with your credit score? Well, grab a coffee (or tea, I don't judge!), and let's dive in.

The Short Answer (Because Who Has Time for Long Answers?)

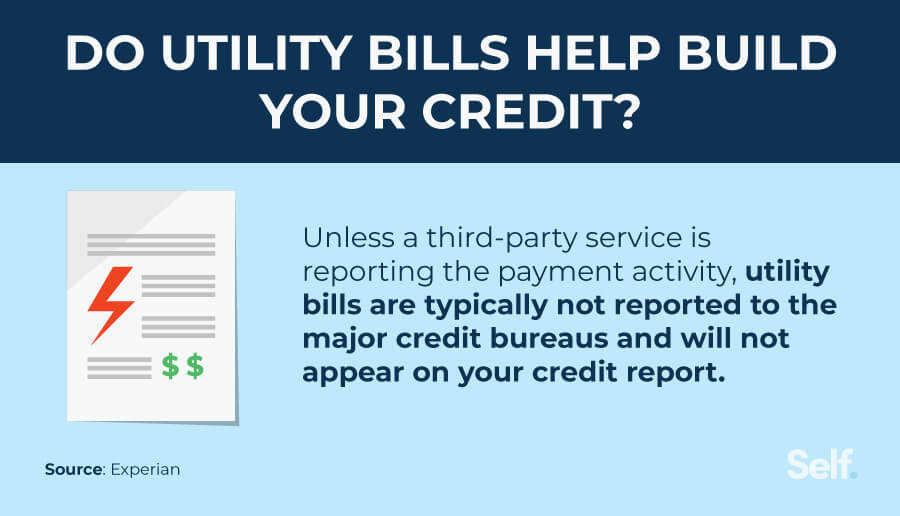

Okay, straight to the point: generally, your on-time utility bill payments won't directly boost your credit score. I know, bummer! It would be amazing if paying for electricity gave us bonus points, right? Imagine the possibilities! Sadly, major credit bureaus (Experian, Equifax, and TransUnion) don't usually track this kind of payment information.

Think of it like this: your landlord doesn't report your rent payments (unless you use a specific rent reporting service), and most utility companies operate similarly. They're not in the business of helping you build credit...they're in the business of keeping the lights on! (And we’re grateful for that! Dark ages are so last century.)

Must Read

But...There's Always a But, Isn't There?

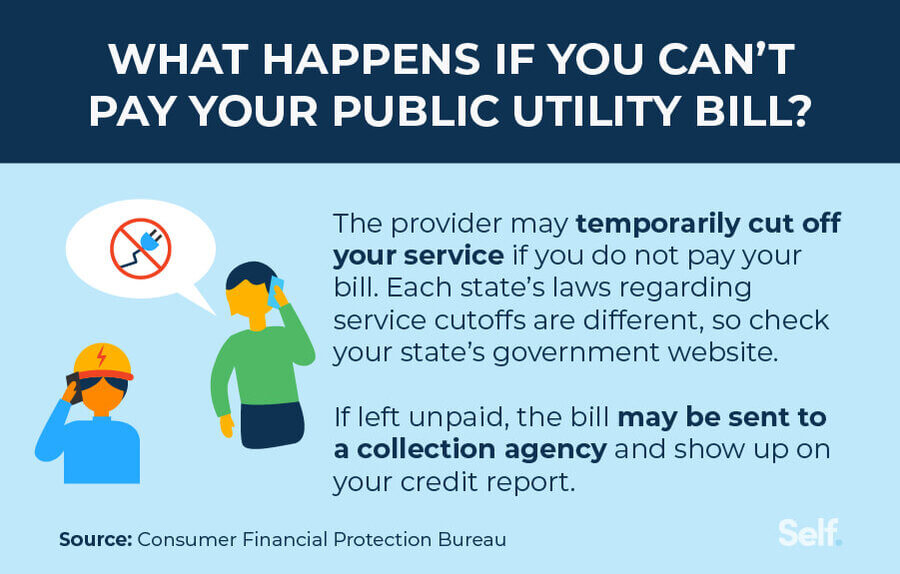

Here's the catch: unpaid utility bills can definitely hurt your credit. Yes, hurt. If you consistently fail to pay your electricity, gas, water, or even internet bills (essential for cat videos, obviously), the utility company might eventually send your debt to a collection agency. And that, my friend, is where the trouble begins.

Collection agencies do report to the credit bureaus. A collections account on your credit report is like a big, flashing neon sign saying "This person doesn't pay their bills!" Not a good look, and it can significantly lower your credit score. Ouch!

So, it's like a one-way street. Paying on time? Meh, no credit boost. Paying late and ending up in collections? Whoa, serious damage. Kind of unfair, right? Like getting a participation trophy for breathing, but penalized for tripping over your own feet.

How Bad Can It Really Be?

A collections account can stay on your credit report for up to seven years. Seven! That's a long time to be haunted by the ghost of unpaid electricity. It can make it harder to get approved for loans, credit cards, and even apartments. Landlords often check credit scores, so that overdue water bill could literally leave you high and dry! (Pun intended. I'm here all week.)

Plus, even after it disappears from your credit report, some lenders might still ask about past collections accounts. So, it's best to avoid them altogether if you can.

Okay, I'm Officially Scared. What Can I Do?

Don't panic! There are things you can do to protect your credit from utility bill mishaps:

- Pay your bills on time, every time. Set up autopay if you're forgetful (like yours truly). Consider it a superhero power: the power to pay on time and avoid collections!

- If you're struggling to pay, contact the utility company. Seriously! Many have hardship programs or payment plans. Explain your situation. They might be more understanding than you think.

- Check your credit report regularly. You can get a free copy from each of the major credit bureaus once a year. Look for any errors or unfamiliar accounts, including collections. If you find something fishy, dispute it!

Think of it as preventative maintenance. Just like you wouldn’t ignore a leaky faucet, don't ignore a late utility bill. Address the issue head-on, and you'll be just fine.

The Uplifting Conclusion (We Made It!)

So, while those on-time utility payments aren't directly showering you with credit score confetti, avoiding late payments and collections is crucial. By staying on top of your bills, communicating with the utility company if you're facing financial difficulties, and regularly checking your credit report, you can protect your hard-earned credit and keep your financial future bright.

And remember, managing your finances doesn't have to be a stressful chore. It's about taking control and making smart choices. You've got this! Now go forth and conquer those utility bills!