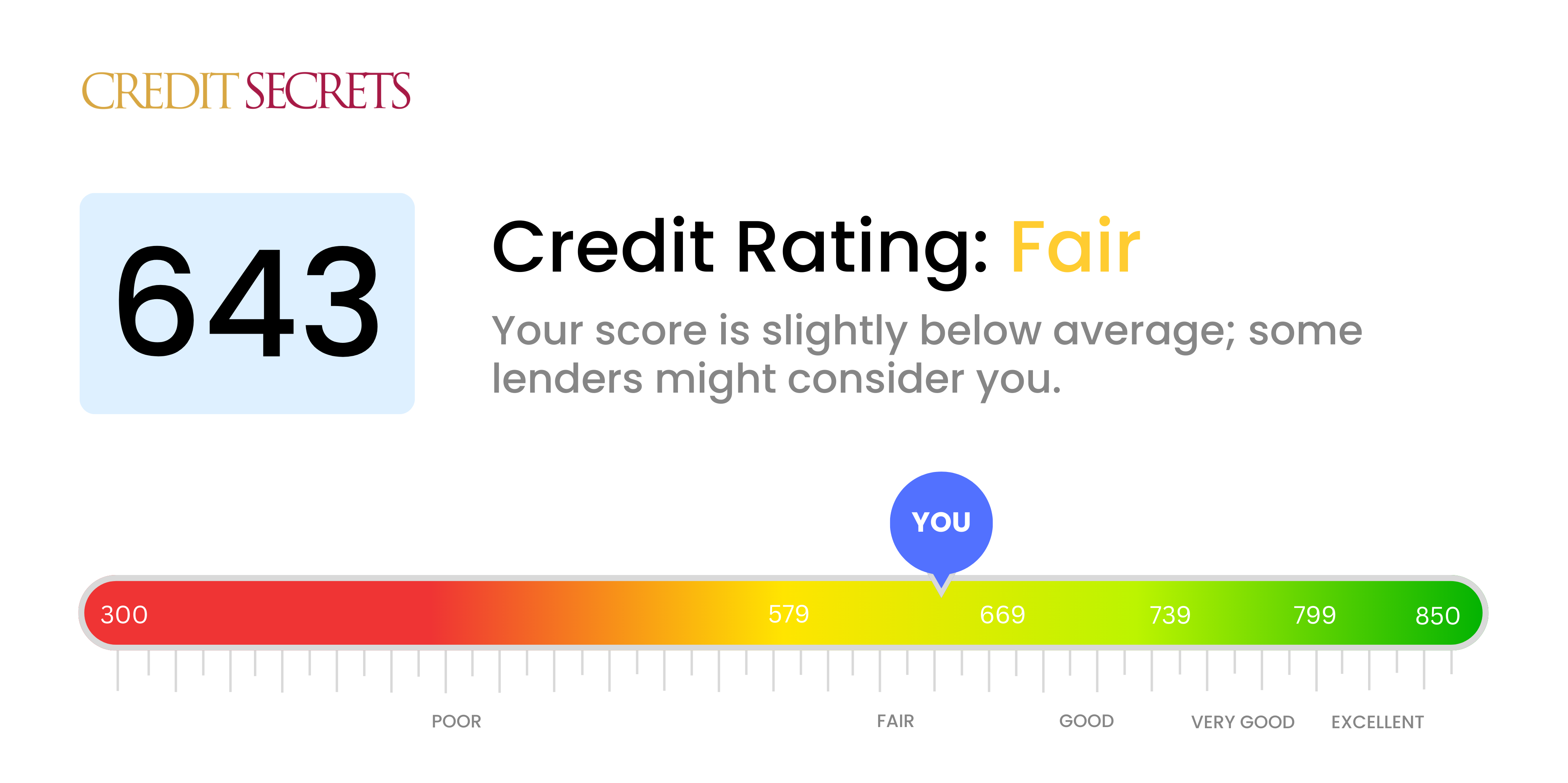

Can I Buy A House With A 643 Credit Score

Okay, let’s talk about something a lot of us dream about: owning a house! It's that cozy picture in our heads – maybe a little garden, a comfy couch, and finally, a place to truly call your own. But then…reality hits. Credit scores. Ugh.

So, the big question: Can you buy a house with a 643 credit score? Let’s break it down, plain and simple. Think of your credit score like a grade in a class. A higher score means you're a good student of money – you pay your bills on time, you don’t max out your credit cards, and you generally handle your finances responsibly. A lower score…well, it suggests there might be room for improvement.

What Does 643 Actually Mean?

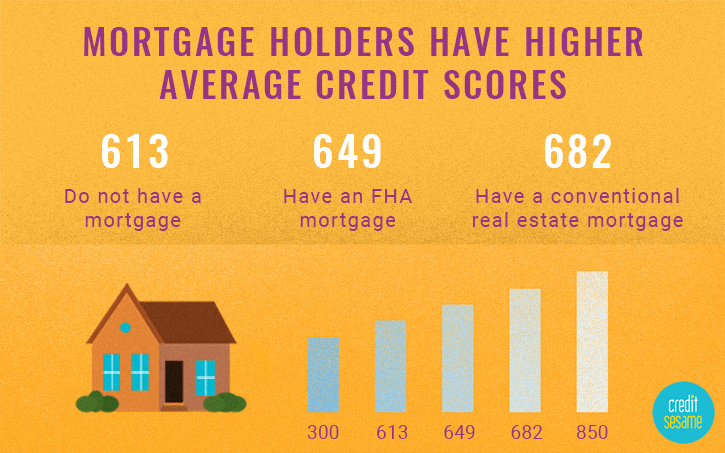

Generally, a 643 credit score falls into the "fair" range. It’s not terrible, but it’s not exactly stellar either. Imagine your score is a pizza. A perfect score is a whole pizza, a bad score is only a slice left, and 643 is like having half the pizza. Edible, but you might still be a little hungry.

Must Read

Now, technically, yes, you can buy a house with a 643 credit score. It’s not an automatic "no." But here's the deal: it's going to be a little more challenging.

Think of it like this: you want to buy that super cool new gaming console. If you have a ton of money saved up, you can just walk in and buy it, no problem. But if you’re a little short, you might need a payment plan (aka a loan), and the store will check your credit to see if they think you're likely to pay them back. The better your credit, the better the terms they’ll offer.

Why Your Credit Score Matters (A Lot!)

Your credit score is like your financial reputation. It tells lenders (banks, mortgage companies, etc.) how risky it is to lend you money. A lower score means they see you as a higher risk. And with higher risk comes higher costs.

Here’s why you should care:

- Higher Interest Rates: This is the big one. With a lower score, you’ll likely get a higher interest rate on your mortgage. This translates to paying thousands more over the life of the loan. Think of it as the price you pay for not having that "whole pizza" credit score.

- Higher Down Payment: Some lenders might require a larger down payment to offset the risk of lending to someone with a lower credit score. This means you’ll need to save up more money upfront.

- Fewer Loan Options: You might not qualify for all the same loan programs as someone with a higher credit score. This limits your choices and could mean settling for a less-than-ideal loan.

Imagine you are buying a car. With a good credit score, you might get a loan with a low interest rate. With a 643, your rates are higher and your monthly payments are going to be bigger. That’s less money for other things, like, you know, fun!

So, What Are Your Options?

Don’t despair! A 643 isn’t the end of the world. Here are a few paths you can explore:

- FHA Loans: The Federal Housing Administration (FHA) offers loans with lower credit score requirements. These are often a good option for first-time homebuyers. However, they usually require mortgage insurance, which adds to your monthly payment.

- Increase Your Down Payment: A larger down payment can make you a less risky borrower, even with a slightly lower credit score.

- Improve Your Credit Score: This is the most effective long-term solution. Take steps to improve your credit score before applying for a mortgage.

Boosting That Score: Easy Peasy!

Improving your credit score isn't rocket science. It’s more like tending to a plant – consistent care and attention will yield results. Here are a few simple steps:

- Pay your bills on time, every time: This is the single most important thing you can do. Set reminders, automate payments – whatever it takes!

- Keep your credit card balances low: Aim to use less than 30% of your available credit. If you have a credit card with a $1,000 limit, try to keep your balance below $300.

- Check your credit report for errors: Mistakes happen! Dispute any errors you find.

- Become an authorized user: Ask a trusted friend or family member with good credit to add you as an authorized user on their credit card. This can help boost your score.

Think of improving your credit like training for a race. You don’t run a marathon without training, right? Similarly, you need to put in the effort to improve your credit score before you apply for a mortgage.

The Bottom Line

Buying a house with a 643 credit score is possible, but it requires careful planning and preparation. Explore your options, improve your credit, and shop around for the best loan terms. Remember, homeownership is a big step, so take your time and do your homework.

And hey, even if it takes a little longer to get there, imagine that moment when you finally get the keys to your own place. Totally worth it, right?