Billing Address On A Debit Card

Have you ever been cruising through an online checkout, ready to snag that perfect gadget or a new book, only to be prompted for your "billing address" even though you're paying with your trusty debit card? It might seem like a minor detail, perhaps a relic from credit card days, but pause for a moment. This seemingly mundane piece of information holds a surprisingly powerful role in keeping your money safe and your online experiences smooth. Let's peel back the layers and uncover the quiet hero that is your debit card's billing address. It's actually quite fun to understand the mechanics behind our everyday digital interactions!

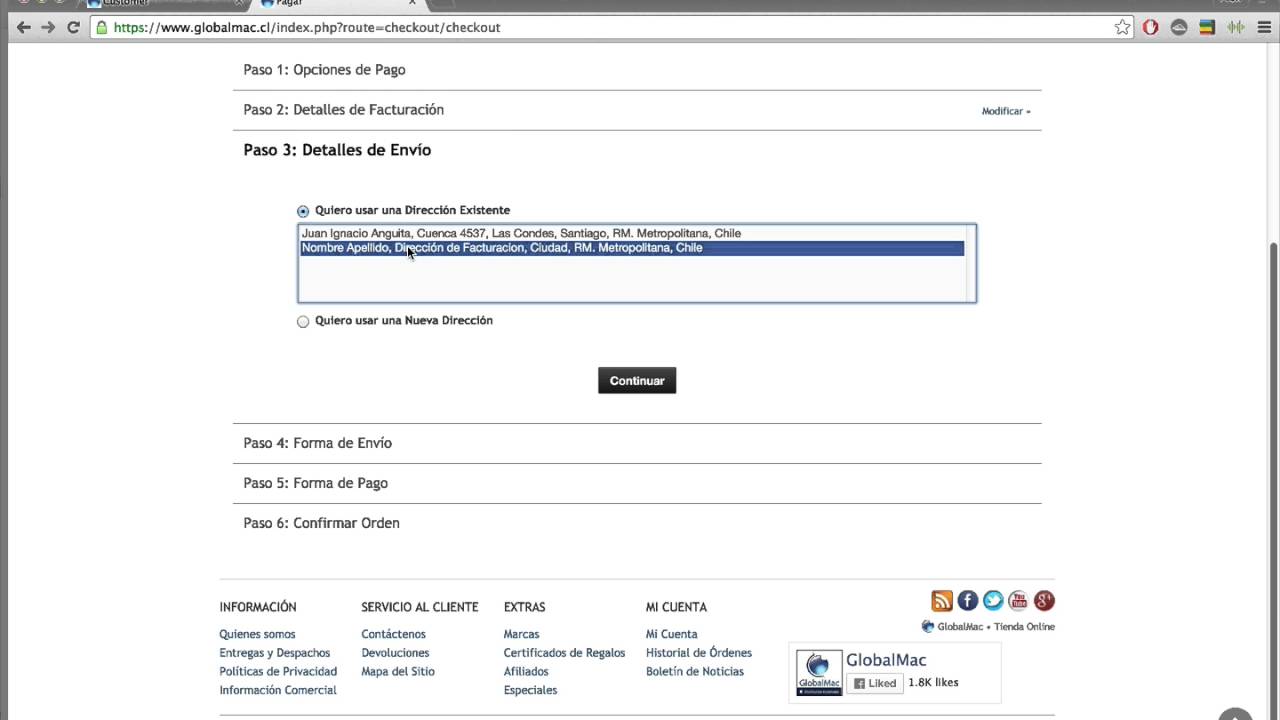

At its core, the billing address serves a critical purpose: security and fraud prevention. Think of it as an extra layer of ID for your debit card. When you make a purchase, especially online, the merchant's payment system sends the address you provide to your bank. Your bank then checks if this address matches the one they have on file for your card. This process is often called the Address Verification System, or AVS for short. If the addresses don't match, the transaction might be flagged as suspicious or even declined. The key benefit here is protection. It helps prevent unauthorized users from making purchases with your card, even if they've somehow gotten hold of your card number and security code (CVV). For merchants, it reduces the risk of fraudulent chargebacks, creating a more trustworthy online marketplace for everyone. It’s a simple yet incredibly effective safeguard that keeps the digital economy ticking securely.

So, where does this invisible guardian appear in our daily lives? Most commonly, you'll encounter it during online shopping for everything from groceries and clothes to digital subscriptions and streaming services. When you book a flight or reserve a hotel online, your billing address is typically requested. Even when setting up recurring payments for utilities or app subscriptions, it’s a standard piece of information. In some specific instances, even physical stores might ask for your billing address – for example, when making a high-value purchase or if their system detects a potential anomaly, providing an extra verification step. In an educational context, understanding the billing address helps us grasp fundamental concepts of digital security, financial literacy, and how payment systems are engineered to protect both consumers and businesses. It's a prime example of how seemingly small details contribute to a robust, interconnected financial world.

Must Read

Ready to explore this concept a bit more practically? Here are a few simple tips. Firstly, always make sure the billing address registered with your bank is up-to-date and accurate. A mismatch is the most common reason for a legitimate transaction being declined. You can usually check and update this through your bank's online portal or by calling customer service. Secondly, if a transaction is declined and you're certain you have funds, double-check the billing address you entered against what your bank has. It's often a simple typo or an outdated address causing the hiccup. Thirdly, next time you're making an online purchase and inputting your address, take a moment to appreciate that this little piece of information is actively working behind the scenes to keep your finances safe. It’s a quiet testament to the sophisticated systems that protect us in our increasingly digital world, turning a mundane field into a powerful guardian of your financial security.