Accrued Interest Paid On Purchases 1099

Okay, picture this: I’m happily clicking away on eBay, found a vintage guitar (don't judge, it's a need, not a want!), and I excitedly smash that "Buy it Now" button. Financing options pop up – enticing, like a siren song. I think, "Why not? Spread out the payments, keep my bank account looking slightly less terrified." Fast forward a year, and I'm getting tax documents everywhere. Then I spot it: a 1099 form…but something's different this time. There’s an amount listed for accrued interest paid on purchases. Cue the internal alarm bells – “Wait, what IS this, and should I be panicking?!”

Turns out, I wasn't alone in my befuddlement. So, let's dive into the wacky world of accrued interest paid on purchases and the dreaded 1099 form. Because knowledge is power, people! And power means not getting blindsided by Uncle Sam.

What Exactly Is Accrued Interest?

In simple terms, accrued interest is the interest that accumulates (hence the name!) on a loan or credit balance over time. It's the price you pay for borrowing money. Think of it like this: you’re renting money, and interest is the rent.

Must Read

Now, when you finance a purchase (like, say, a gorgeous vintage guitar), the lender (like PayPal Credit, Affirm, Klarna, or whoever) charges you interest. This interest accrues daily, monthly, or however their little calculator decides to whirr. And that interest eventually gets paid as you make your payments. No surprises there, right?

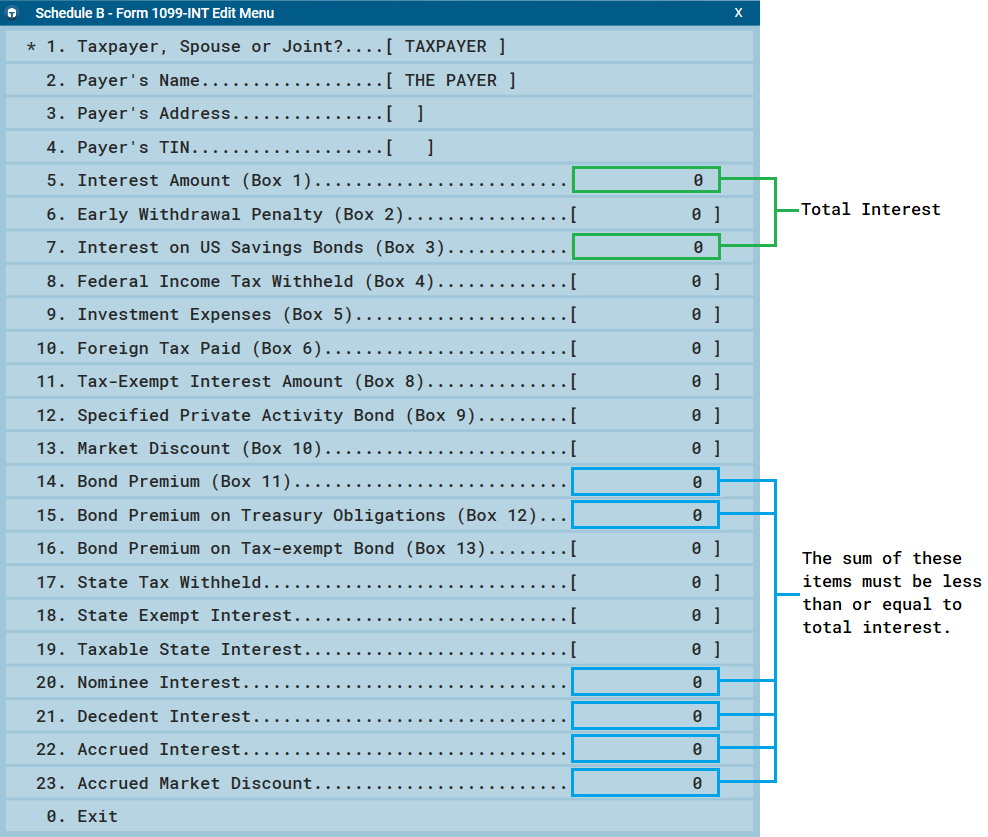

But here's the key: if you pay a certain amount of interest throughout the year, the lender is required to report that to the IRS. This reporting is typically done on a 1099 form, specifically a 1099-MISC or 1099-INT, depending on the exact situation. (Don't quote me on the exact form, tax laws are more tangled than my guitar strings!)

Why Am I Getting a 1099?

So, why do you get a 1099 for accrued interest paid on purchases? The IRS wants to know about income (and, in this case, deductible expenses). Basically, they're saying, "Hey, we see you paid some interest. We want to make sure it's reported correctly."

The threshold for receiving a 1099-INT (for interest) is usually pretty low – often just $10 or more. (Check the IRS website for the exact current threshold – it's subject to change, because…well, it's the IRS.) So, even if you only financed a relatively small purchase, you could still receive a 1099.

Here's the kicker: in some situations you might get the 1099-MISC instead of the 1099-INT. The important thing is that you got something reporting interest payments. If you're not sure which form applies to your situation, consulting a tax professional is always a good idea.

Okay, What Do I Do With It?

Don’t panic! (I know, easier said than done when taxes are involved.) Here's what you do:

- Verify the Information: Double-check that your name, address, and taxpayer identification number (usually your Social Security number) are correct on the form. If there are any errors, contact the lender immediately to get a corrected form.

- Keep It For Your Records: This is crucial. You'll need this information when you file your taxes.

- Enter It on Your Tax Return: Depending on the specific tax form you use, you'll likely need to enter the amount of interest paid somewhere on your tax return. Tax software programs typically guide you through this process. Again, when in doubt, consult a professional.

- Consider Deductibility: In some cases, the interest you paid on purchases might be tax-deductible. (Yay!) However, this often depends on the type of loan and how you're using the purchased item (business vs. personal use). Again, this is where a tax pro can really help.

Is This Something to Worry About?

Usually, no. Receiving a 1099 for accrued interest isn't inherently bad. It just means you need to report it on your tax return. However, if you don't report it, the IRS might notice the discrepancy and come knocking. (Trust me, you don't want that.)

The biggest thing to remember is to keep accurate records and report all income and deductible expenses honestly and accurately. And maybe, just maybe, think twice before hitting that "Buy it Now" button with financing options...unless it's a REALLY awesome vintage guitar.

Disclaimer: I'm just a person who likes guitars and avoids tax audits. This isn't tax advice. Always consult with a qualified tax professional for personalized guidance.