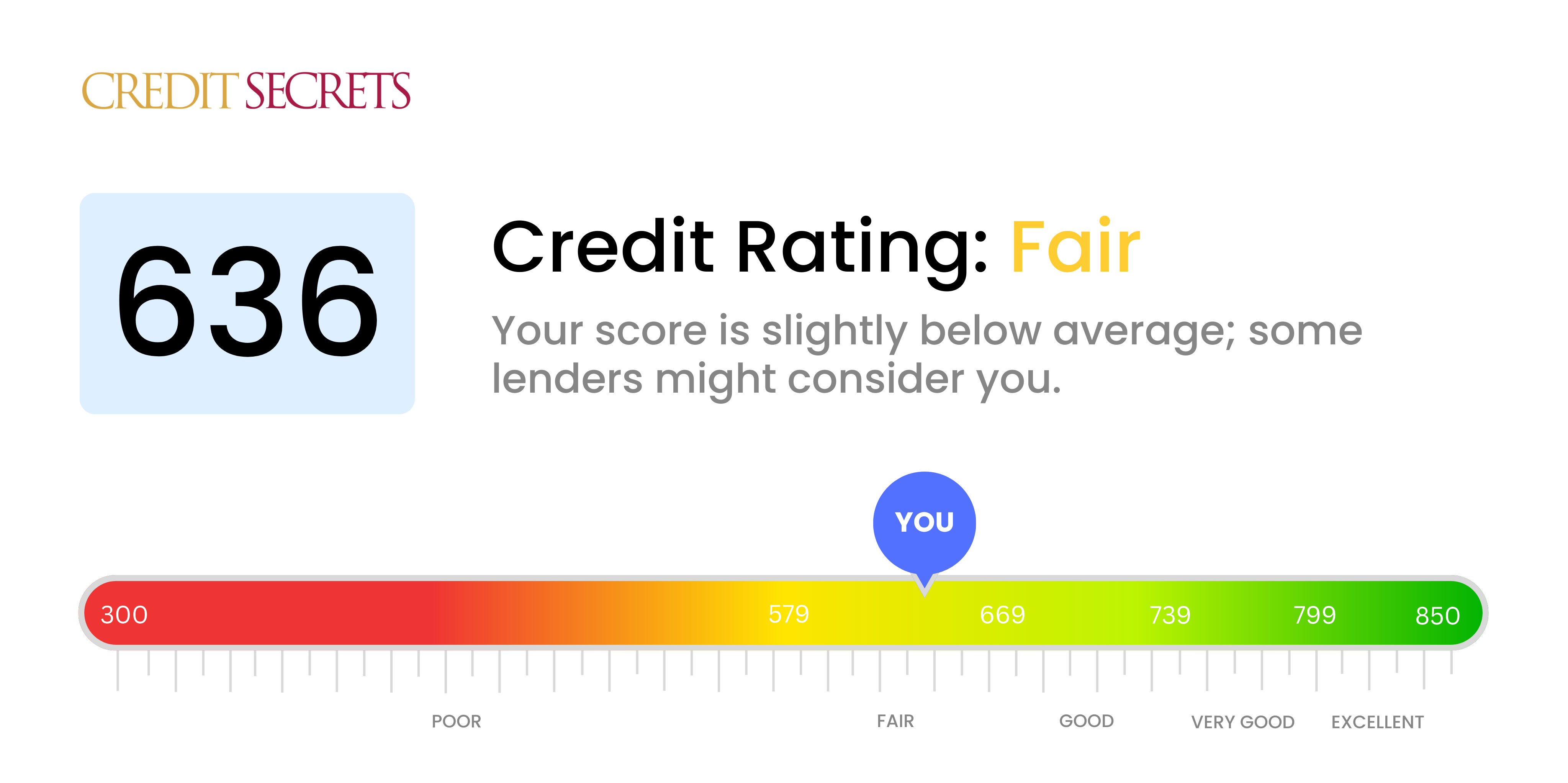

636 Credit Score Good Or Bad

Okay, let's talk about credit scores! Specifically, the magical number 636. Is it your financial fairy godmother, or more like a mischievous goblin hiding under your bridge? Don’t worry, we'll decode it together!

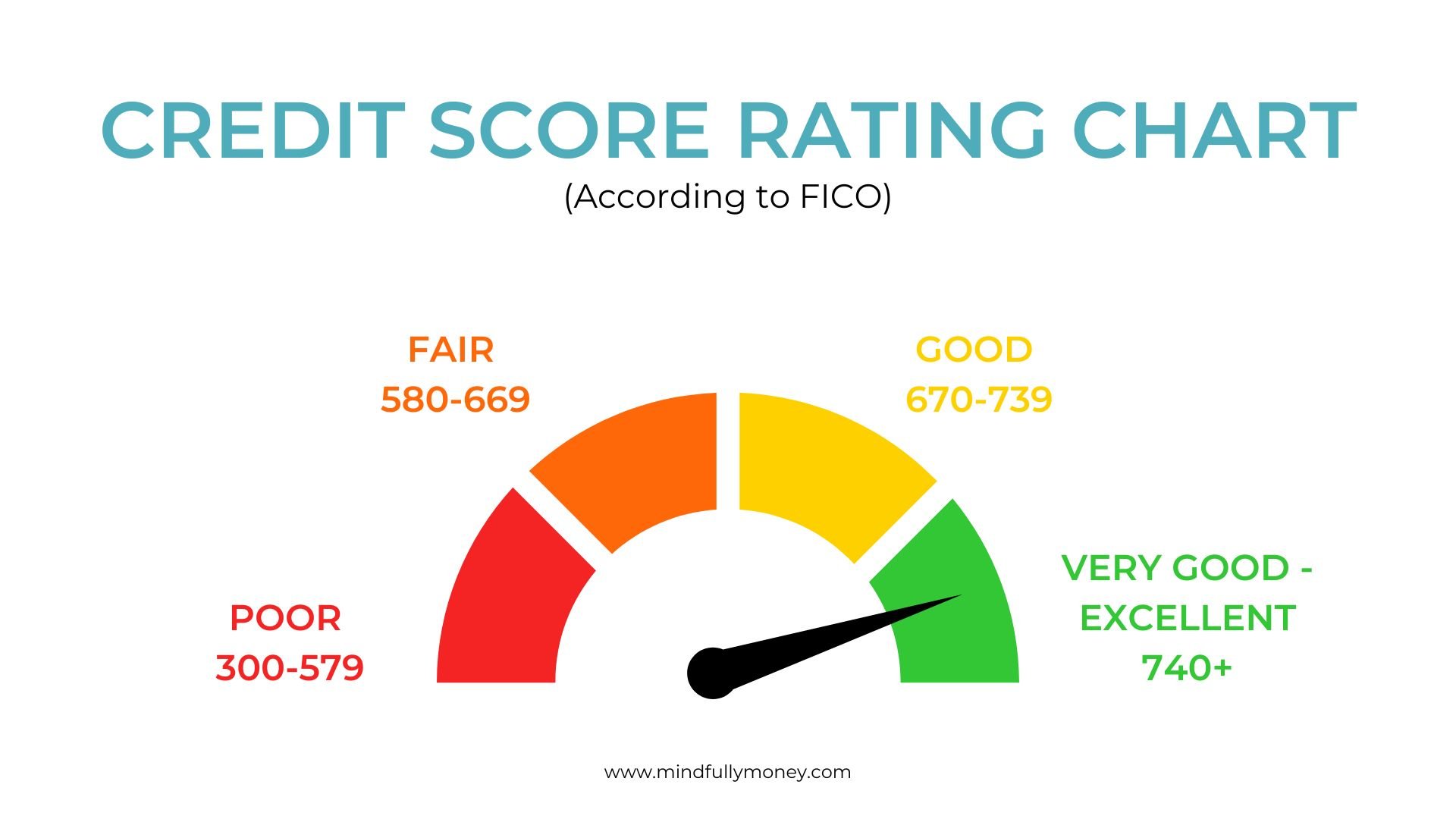

The Credit Score Spectrum: Where Does 636 Land?

Think of credit scores like a popularity contest for your financial responsibility. The higher the score, the more lenders want to be your friend. Generally, the scale runs from 300 to 850.

So, where does 636 fit in? It’s in the "Fair" zone. Think of it as being invited to the party, but not quite being the life of it… yet!

Must Read

Decoding "Fair": Not Bad, But Not Rockstar

“Fair” means you’re not in terrible shape. You’re not doomed to a life of ramen and carrier pigeons. But it's also not a golden ticket to instant approval for that dream house or fancy sports car you've been eyeing.

Basically, you're on the right track, but there's definitely room for improvement. Imagine it like this: you’ve started training for a marathon, you're past the "couch potato" stage, but you're not quite winning any races yet.

What Does a 636 Credit Score Mean in Real Life?

Let's get down to brass tacks. How does this number actually affect your life? Well, it's all about access and interest rates.

When you have a 636 credit score, you can probably still get approved for loans and credit cards. But here’s the kicker: those loans and credit cards are likely to come with higher interest rates.

Think of interest rates as the price you pay for borrowing money. A higher interest rate means you'll pay more over the life of the loan. It's like paying extra for guac at Chipotle... only way more expensive!

For example, let's say you want to buy a car. With a 636 credit score, you might get an interest rate of, say, 8%. Someone with a super-duper credit score (like 750+) might snag an interest rate of only 4%.

Over the course of a five-year loan, that difference can add up to thousands of dollars! That's a lot of guac… or, you know, a down payment on a small island.

The Good News: You Can Totally Improve Your Score!

Don't despair! A 636 credit score isn’t a life sentence. It’s just a starting point. Think of it as a "work in progress" sign on your financial future.

The great news is that improving your credit score is totally doable. It takes time and effort, but it's like planting a money tree. With the right care, it'll blossom!

Simple Steps to Boost Your Credit Score:

Here's the magic formula, broken down into bite-sized pieces:

Pay Your Bills on Time, Every Time! This is the golden rule of credit scores. Late payments are like throwing rocks at your financial reputation. Set reminders, automate payments… do whatever it takes to avoid those dreaded late fees!

This includes everything: credit card bills, utility bills, student loans, even that subscription to "Exotic Cheese Monthly" (if you have one!). Treat every bill like it's the most important thing in the world… financially speaking, it kind of is.

Keep Your Credit Card Balances Low. This is known as your credit utilization ratio. Ideally, you want to use less than 30% of your available credit. So, if you have a credit card with a $1,000 limit, try to keep your balance below $300.

Imagine your credit card limit as a glass of water. You don't want to fill it to the brim, right? Lenders see that as a sign you're relying too heavily on credit. Keep it around a third full, and you'll look much more responsible.

Become an Authorized User. If you have a responsible friend or family member with a credit card and a good credit history, ask them to add you as an authorized user. Their good habits can rub off on your credit score! Just make sure they actually are responsible!

A Complete Guide to Your Credit Score

This is like getting a free piggyback ride to a better credit score. Their positive payment history will be reported to the credit bureaus under your name, giving you a boost. Just be careful not to abuse the privilege, or you might strain the friendship!

Don't Open a Bunch of New Credit Cards at Once. Applying for too many credit cards in a short period of time can ding your score. Each application triggers a "hard inquiry" on your credit report, which can lower your score slightly.

It looks like you're desperate for credit, which can make lenders nervous. Think of it like speed dating for credit cards… it's better to take your time and find a good match than to swipe right on everyone!

Check Your Credit Report Regularly. You're entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year. Review it carefully for any errors or inaccuracies. Even small mistakes can hurt your score.

Think of your credit report as a financial resume. You want to make sure it's accurate and up-to-date. Dispute any errors you find… it's like correcting a typo on your job application!

Patience, Grasshopper!

Improving your credit score isn't an overnight process. It takes time and consistency. But with a little effort, you can definitely move from "Fair" to "Good" to even "Excellent!"

Think of it like learning to play the ukulele. You won't become a rock star overnight, but with practice and dedication, you'll be strumming sweet tunes in no time!

So, 636: Good or Bad? The Verdict!

The final answer? 636 is... neither terrible nor fantastic. It's a stepping stone! It’s a “room for improvement” kind of score.

It's a sign that you're on the right track, but there's still work to be done. Embrace the challenge, follow the tips above, and watch your credit score climb! You've got this!

Remember, your credit score is just a number. It doesn't define you. But it can open doors to better financial opportunities. So, take control of your credit, and start building a brighter financial future today! You might even be able to afford that small island sooner than you think!

Now, go forth and conquer your credit! And maybe lay off the exotic cheese subscription for a while. Just a thought!