595 Credit Score Car Loan

.png)

Okay, picture this: you’re stranded. Not on a desert island (though that would make for a much more exciting story, right?), but on the side of the road with a sputtering engine and the distinct smell of burnt… something. My friend Sarah was in this exact situation last month. Her trusty (or, you know, not-so-trusty) hatchback finally gave up the ghost. Now, Sarah’s a responsible adult… mostly. But her credit score? Let’s just say it’s seen better days. A 595, to be exact. And she needed a car. Stat.

So, can you actually get a car loan with a credit score hovering around 595? The short answer? Yes, absolutely. But like most things in life, there’s a “but.” A big "but", actually.

We're diving deep into the world of 595 credit score car loans. Buckle up, buttercup; it’s going to be a bumpy ride. (Sorry, had to!)

Must Read

What's the Deal with a 595 Credit Score?

First things first, let’s be real. A 595 credit score isn’t exactly winning any awards. It falls squarely into the “fair” or “poor” credit category. This basically means lenders see you as a bit of a risk. They're thinking, "Hmm, this person might not pay us back on time... or at all!"

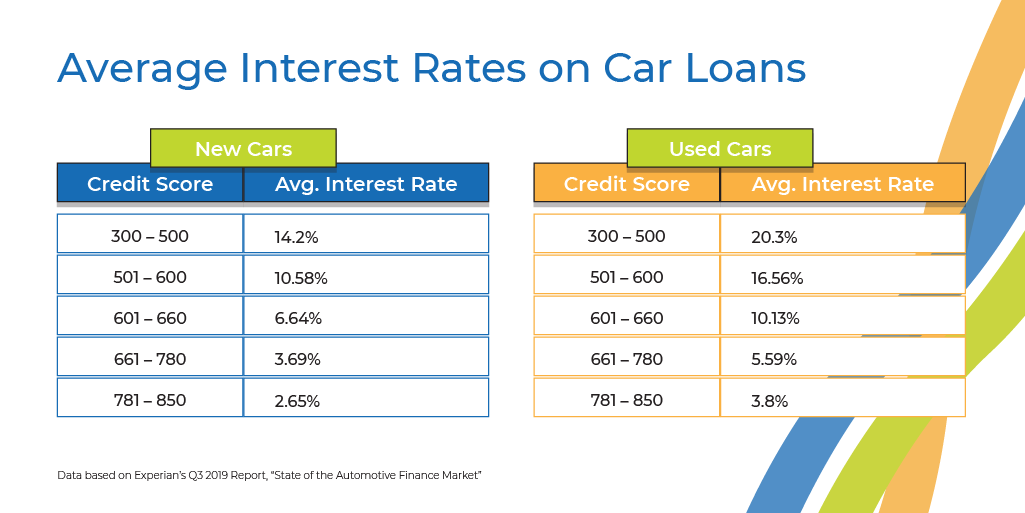

And what happens when lenders see you as risky? Higher interest rates, my friend. Prepare yourself.

Think of it like this: you’re asking someone to lend you a significant amount of money. They're more likely to say "yes" if you have a history of paying back debts responsibly. A low credit score is like showing up to that conversation wearing a clown suit and juggling flaming torches. It's attention-grabbing, but not in a good way. (No offense to clowns. Some of them are probably very responsible borrowers!).

Getting Approved: It's Possible (But Prepare for the "Ouch" Factor)

Okay, so you're in Sarah's shoes (or, you know, your own shoes). You need a car, but your credit score is whispering sweet nothings of "denial" into your ear. Don't despair! Here’s the lowdown on securing that loan:

- Expect Higher Interest Rates: This is the big one. Lenders are taking a chance on you, so they’re going to charge you more for the privilege. Be prepared for interest rates that are significantly higher than what someone with excellent credit would get. (Think "ouch" level pain)

- Down Payment is Your Friend: A larger down payment shows the lender you’re serious and reduces their risk. Plus, you'll be borrowing less money, which translates to lower monthly payments. Aim for at least 10% if you can swing it.

- Shop Around. Seriously.: Don’t just go to the first dealership you see. Get quotes from multiple lenders, including banks, credit unions, and online lenders specializing in bad credit loans.

- Consider a Co-Signer: If you have a friend or family member with good credit who's willing to co-sign the loan, it can significantly increase your chances of approval and potentially lower your interest rate. (But make sure you can actually make the payments! Don't ruin your relationship over a car!)

- Improve Your Credit (Even a Little Helps): Paying down other debts, correcting errors on your credit report, and avoiding any new credit applications can all help boost your score, even if it's just a few points. Every little bit counts!

The Fine Print: What to Watch Out For

When you're desperate for a car, it's easy to get caught up in the excitement and miss crucial details. But trust me, reading the fine print is non-negotiable.

- Watch Out for Predatory Lenders: Some lenders prey on people with bad credit, offering loans with ridiculously high interest rates and hidden fees. Steer clear of these vultures! If something sounds too good to be true, it probably is.

- Consider a Used Car: A brand-new car depreciates quickly, meaning you’ll be paying off more than the car is actually worth in the early years. A reliable used car is often a much smarter choice.

- Think About the Total Cost: Don’t just focus on the monthly payment. Look at the total cost of the loan, including interest, fees, and any other charges. You might be surprised how much more you’re paying in the long run.

Sarah, after some serious shopping around and a healthy dose of financial soul-searching, managed to secure a loan on a decent used car. Her interest rate wasn't pretty, but she knew it was a temporary situation. She's now diligently making her payments and working on improving her credit score so she can refinance in the future.

Getting a car loan with a 595 credit score isn't easy, but it's definitely possible. Just remember to do your research, shop around, and be prepared for the higher costs associated with bad credit. And hey, who knows? Maybe one day you'll be writing an article about how you boosted your credit score and landed that dream car. Now that would be a story worth telling!